Saturday, May 16th, 2026

Laramie, Wyoming

By Dan Denning

Uh oh. Don’t look now, but the yield on the 30-year US Treasury Bond is back over 5%. In the recent past, that’s been a warning signal from markets. But a warning for what?

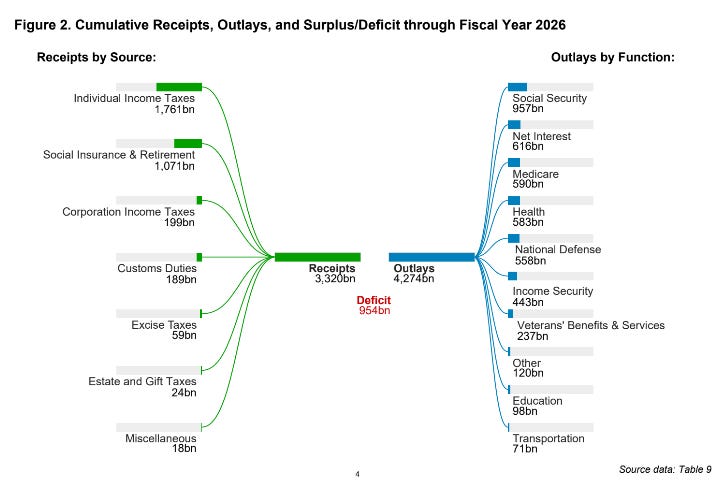

First, that there are serious doubts about the ability of the Fed to control inflation or Congress to control spending. Almost $10 trillion worth of the US national debt—more than a third of all the debt held by the public—must be refinanced this year.

At higher interest rates, the interest expense on that debt will climb to over $2 trillion (the feds have spent over $600 billion on interest payments halfway through the fiscal year, which is the second most expensive item in the federal budget behind Social Security payments). And the government is on pace to rack up another $2 trillion in NEW debt this year.

Here’s the thing though. Higher interest rates aren’t just bad for bonds (as rates go up, bond prices go down) and borrowers. They’re bad for stocks too. Why?

In theory, higher interest rates raise the so-called ‘risk free’ rate of return on bonds (with $40 trillion in debt, there is serious doubt about whether US government bonds are ‘risk free,’ but bear with me). The higher ‘risk free’ rate in turn raises the ‘discount rate’ used in valuation models to price stocks. In simple terms, as the discount rate goes up, future cash flows are worth less today.

That’s why it’s bad for stocks. In fact the only way out of it is for fast-growing companies to grow earnings even faster. This means the mega-cap ten tech stocks driving this rally (AI plays) have to grow even faster…or be repriced. Repriced….lower.

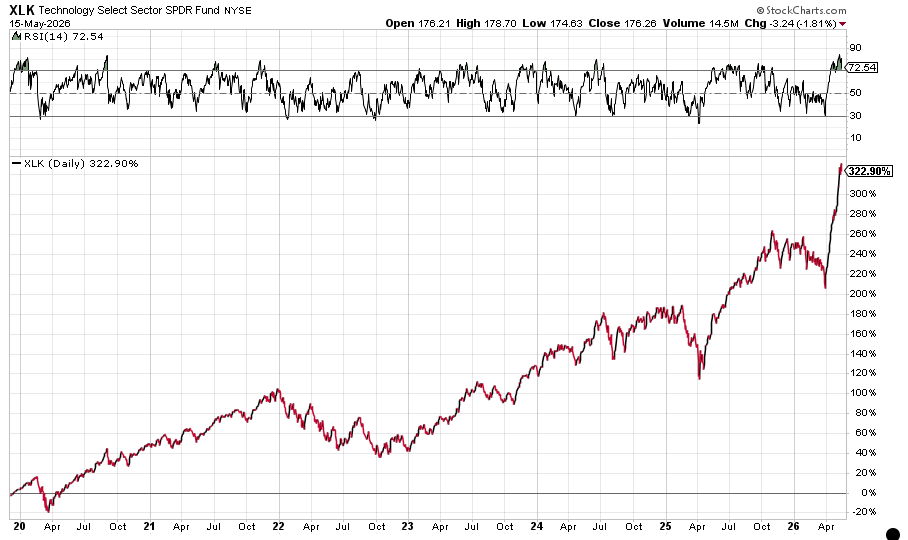

It’s a long way down from here. Did you know that since the lows in mid-March, the S&P sector (XLK) is up almost 40%? That’s 40% in about six weeks! The only other time that’s ever happened is in the six weeks or so after the Covid lows in March of 2020…and AI wasn’t even really a ‘thing’ then.

This market is NOT priced for higher interest rates, which would push the discount rate up even further. Yet the inflation numbers this week (CPI and PPI) both showed that inflation is running hot. New Fed Chair Kevin Warsh has his hands full (his first meetings as head of the Federal Open Market Committee is June 16th-17th…and futures markets say that there is a 64% probability that the Fed will have to HIKE interest rates before the end of the year.)

The President will go apoplectic if the Fed raises rates this summer. The closer it is to the mid-term elections, the more politically sensitive each Fed interest rate decision is. The smart money is on the Fed to do something sooner rather than later. What should YOU do in the meantime?

The BPR view on what you should do has not changed. Please review Investment Director Tom Dyson’s note from Wednesday if you haven’t already. Tom reckons the most likely way out of a debt bomb is currency debasement. That’s what we’re positioned for.

Are you?

Until next week,

Dan

P.S. Our friends at International Living believe gold’s next surge will take it to $10,000/oz. On Monday, they’re hosting a ‘masterclass’ for investors and speculators looking to profit. If that sounds like you, you can sign up here.

I continue to be amazed that the men and women elected to high office (President and Congress simply refuse, year after year regardless the political party in power, to reduce spending.

Jimm,

Unless their constituents feel the pain of inflation, like Argentina did, they will not accept the cuts needed. Our elected congress like to keep their jobs and cutting the budget is a sure way to lose officce.