Your money is no good here

With the Genius Act and the new implementing regulations, your money will become ‘programmable’...with algorithms in the money itself that will dictate, automatically, what you can do with it.

Monday, April 20th, 2026

Bill Bonner, from Baltimore, Maryland

‘It is basically a way to keep you in an open-air prison.’

--Catherine Austen Fitts

Over the weekend, the world’s attention was on the US/Israeli war against Iran...and Lebanon. Was it on, or off? The strait of Hormuz...open, or closed?

While these things dominated the headlines...the feds quietly stitched more pieces onto their Frankensteinian new money system.

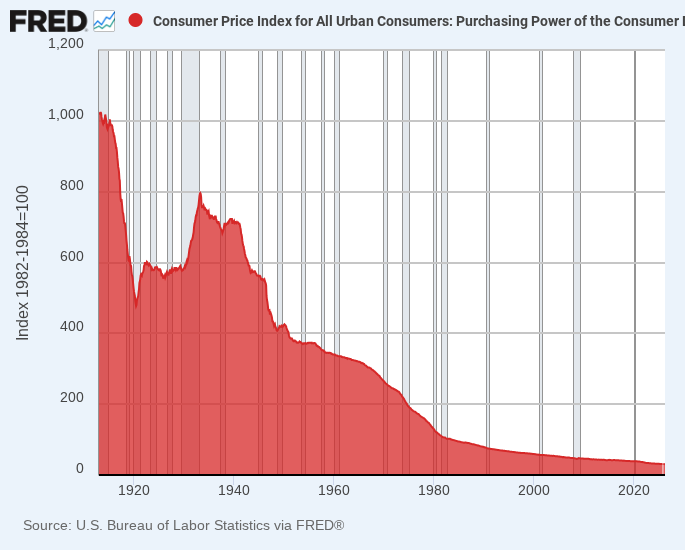

It reminded us of 1971. That was the fateful year that President Richard Nixon, aided and abetted by the top ‘conservative’ economist of the time, Milton Friedman, created the new, fake dollar...which has twisted the economy and added an excess of $80 trillion to America’s debt burden.

At the time, 55 years ago, only a few cranks and crackpots even noticed. The Nixon team disguised the major change with a minor one. It announced wage-price controls on the same evening; they were so preposterous that they absorbed almost all the media’s attention and were withdrawn soon after. But the new money is still here…now in its 55th year. We presume that the all-time high in bond yields — achieved in July 2020 — marked the beginning of the end. The dollar has lost 99% of its value (against gold) so far; now it will lose the rest.

And now that this Funny Money Era (FME) approaches its denouement...what new monstrosity, hidden by the fog of war, slouches into Washington?

Already in place, in July 2025, was the “Genius Act” preparing stablecoins for entry into the mainstream financial system. And now comes this...MN Gordon:

On April 8, 2026, less than 10 days ago, while most people were distracted with bombs dropping on Iran, the U.S. Treasury, its Financial Crimes Enforcement Network (FinCEN), and the Office of Foreign Assets Control (OFAC) issued a joint proposed rule to implement provisions of the GENIUS Act. This rule formally integrates stablecoins into the Bank Secrecy Act (BSA).

According to Treasury Secretary, Scott Bessent, “This proposal will protect the U.S. financial system from national security threats without hindering American companies’ ability to forge ahead in the payment stablecoin ecosystem.”

What does this mean? We don’t know either. So, we turn back to Mr. Gordon:

‘This, in essence, establishes a permanent digital leash that can be used to control your behavior. As these regulations tighten, the wall between your private wealth and federal oversight disappears. Every transaction you make will be visible to a centralized authority.’

Nixon began the FME when he turned the real dollar (backed by gold) into a phony dollar (backed by nothing). Real money must not be subject to manipulation by its issuers. It must also be something you can hold, free and clear.

Imagine that you sell tomatoes and receive a gold coin in return. Transaction complete. You earned your money, now you can do with it as you please. Instead, imagine that there is an invisible code embedded in the coin...so that it can only be used to buy an EV or a MAGA hat! This is the next phase of the Funny Money Era. Not only is the money fake...the feds are aiming to use it to control you.

The feds have been attaching strings onto your money for years. Money Laundering provisions, ‘Know Your Customer’ rules, ‘suspicious activity’ reports...and now with the Genius Act and the new implementing regulations, your money will become ‘programmable’...with algorithms in the money itself that will dictate, automatically, what you can do with it.

At the international level, foreign firms earned dollars by selling products to Americans. Then, like trip wires to a land mine, they saw the strings attached. Their money could be seized or sanctioned...and they could be cut off from the world’s SWIFT money transfer system. That’s why foreign nations are looking for alternatives to the dollar system.

Probably the most visible single case is that of Francesca Albanese. The UN gave her the job of reporting on the treatment of Palestinians. Her report was critical of Israel. And now it is she who is mistreated. El Pais:

Her visa was revoked...all her assets were frozen, including her bank account and her apartment in the United States, even though she now lives in Tunisia.

In addition, she was placed on a blacklist that effectively cuts her off from the entire international banking system, as if she were a terrorist or a drug trafficker. Penalties were also established for any U.S. citizen who engages in financial or in-kind transactions with her — including, for example, her husband, who works at the World Bank, and her daughter. “In theory, they can’t even invite me for a coffee, because they could be fined up to $1 billion or face up to 20 years in prison...”

Only people with the ‘right’ opinions will be allowed to voice them. Otherwise, they could be cut off from their money.

And the system will managed, not by Congress, the courts or even the Fed…but by AI. So, when your back account is blocked and your credit card doesn’t work...you will try to find out why. What charges were filed? What court found you guilty? Who is responsible?

“We’re sorry but the purchase you are attempting to make is not authorized,” will come the answer.

Regards,

Bill Bonner

I awakened today to hear that there are rumblings that the US is going to eliminate the nickel, just like I (among others) predicted was going to happen soon after eliminating the production of the penny. The stated reason is that it costs more to make than the 5 cents it is supposedly worth.

My complaint when the GENIUS Act was passed was that it was a fast step toward digital currency. Not digital money; there's no such thing. Digital currency is what can be programmed, with no direct input of the user.

Just think what can happen when a truly evil regime comes to power!

WOW Bill, what a nice thought to start the week. I seem to hear George Orwell laughing somewhere in the background.

Jim Marshall