Friday, July 10th, 2026

Laramie, Wyoming

By Dan Denning

Happy statehood day Wyoming!

On this day, July 10th, in 1890, Wyoming became the 44th State in the Union. Jubilee Days in Larimie at the moment. Big parade and pancake breakfast tomorrow. But nice work on becoming a state 136 years ago, Wyoming. President Benjamin Harrison admitted it. And as it turns out, there are some things we could learn from 1890 and President Harrison. More on that shortly.

First, the clowns, charlatans, and counterfeiters at the Federal Reserve have released their semi-annual Monetary Policy Report. The paper argues that inflation expectations are ‘anchored’ at 2%. Which is funny because in the same report, the Fed says that Personal Core Expenditure inflation is actually at 4.1% for the last twelve months.

You wonder who the Fed is asking about inflation if it concludes inflation expectations are ‘well anchored’ at 2%. They’re not asking anybody who buys gasoline or groceries. Or pays for insurance, tuition, or prescription drugs. And keep in mind that a policy goal of maintaining 2% inflation is not ‘price stability.’ It’s a slow-drip devaluation in the purchasing power of your savings…by design.

The report went on to ‘blame’ inflation on three things: tariffs, high energy prices, and supply-side shocks from the AI/data-center build out. Meh. The only one of the three for which there is real evidence is high energy prices. And those are almost entirely related to the ongoing war/cease fire/war in Iran.

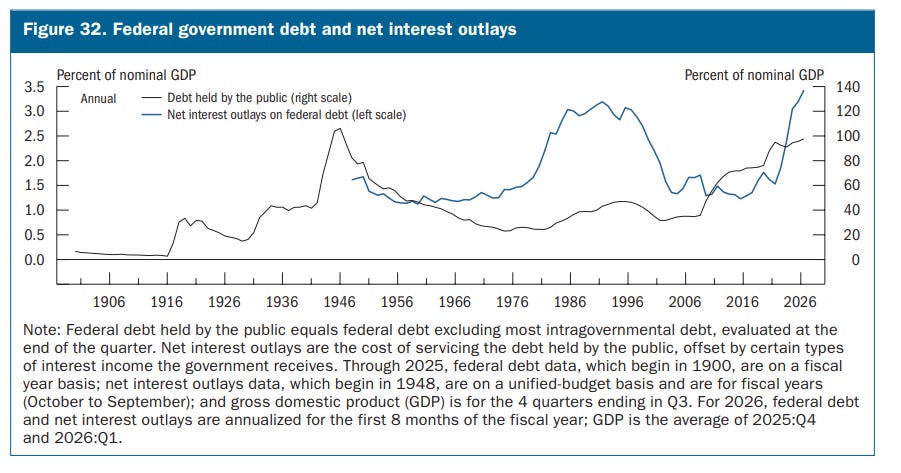

Notably, the Fed did not blame itself for inflation. But the paper indirectly admitted the Fed’s role in undermining sound money by publishing the chart at the top of this week’s note. The chart shows a sharp spike in US government debt held by the public beginning in 1913, which was the year the Fed began perverting US money in earnest.

Huge US annual deficits and public debt equal to 100% of GDP are not possible without the Fed’s intervention in the market. It creates money to buy bonds from banks. It also directly buys bonds issued by the Treasury. The Fed is the beating heart of the US Welfare/Warfare State. But you won’t read that in the report.

The scariest line on the chart is the rise in net interest expense on the debt since 2020. A trillion dollars a year is one thing. That’s the nominal amount (more or less) of annual interest expense on $40 trillion in debt. That’s about 3.5% of GDP. If Bill is right (and he is) about the Primary Trend being higher interest rates, the US is going to spend a lot more money in the coming years just paying interest on debt. Even a small increase in interest rates will be a big problem.

A BIG increase–the kind caused by a failed Treasury bond auction or the fear of massive money printing–well that will be a death sentence for the dollar, executable immediately. The Fed appears to prefer a slow, managed decline–the kind you will barely notice unless you’re paying attention. Pay attention. And don’t forget to buy the dip in precious metals!

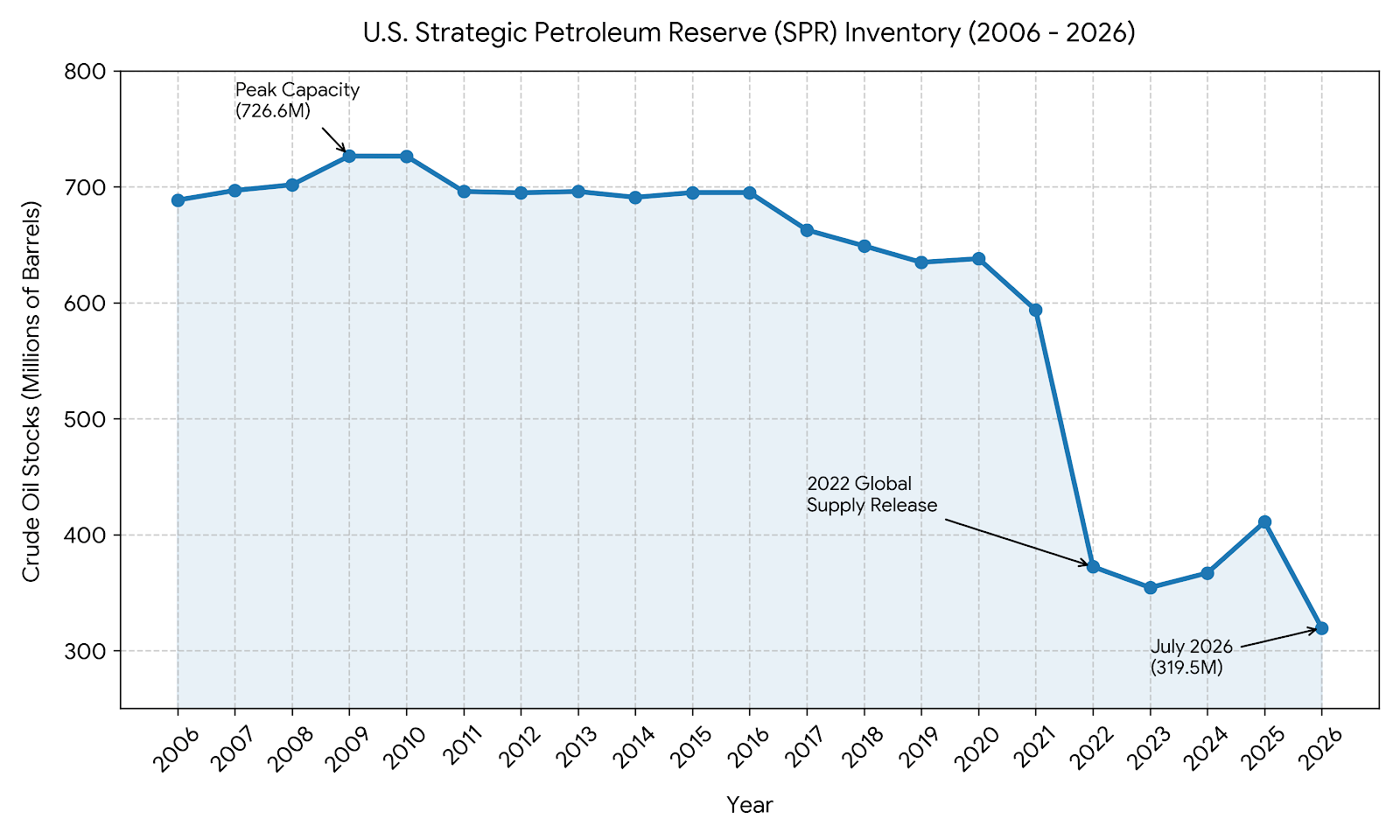

When is a Strategic Petroleum Reserve no longer a reserve? There are about 320 million barrels left in the reserve at the moment. That number is critically low and getting lower. When will it stop? When does it HAVE to stop? First some context.

The Biden draw-down in the SPR—ostensibly to compensate for the ‘oil shock’ at the beginning of the Russia/Ukraine war in 2022 (but also about lowering gas prices before the US mid-terms) was 180 million barrels. The Trump draw-down has been around six million barrels per week and now sits at a total of around 172 million barrels.

By the time the next official data comes out, the Trump draw-down will exceed the Biden draw-down and the Reserve will be at its lowest level since 1983. Again, how low can it go?

The answer is determined by how oil in the SPR is stored and released. It’s stored in underground salt caverns. It’s released by pumping briny water into those caverns. Highly saturated salt water has a much higher density (specific gravity) than oil. Pumping the water into the cavern displaces the crude oil up, forcing it out at the top.

But there’s a catch.

Even briney sea water can alter the structure of the caverns in which the SPR resides. It mixes and erodes or distots the walls of the cavern. Below 300 million barrels, the government says the salt cavern structures become less stable with the added water. At current rates of depletion, that means in about three weeks, the Administration will have to decide whether to go below 300 million barrels…or buy oil on the open market. Or do something. Or do nothing and hope for the best.

Congress hasn’t been helpful (when IS it helpful?) In 2017, it began using the SPR as a piggy bank by selling oil to fund special government projects. It failed to replenish the Reserve when oil prices were low (something Trump suggested in his first term…but wasn’t done because mostly Democrats said it would be a subsidy to ‘big oil.’)

The statutes on the books say the Reserve can never go below 150 million barrels. We’re a long way from that (about 24 weeks according to current draw-down rates). Will we still be engaged in a special military operation in Iran in 24 weeks? Will other transit options that bypass the Persian Gulf entirely be available by that time? What will the oil price be?

Nobody knows. But in the meantime, we’re quite happy with our positions in uranium, oil and gas, and other real assets that throw off a stream of income. New readers can catch up quickly by reading Investment Director Tom Dyson’s July Monthly Strategy Report.