If not now, when?

A sustained drop in interest rates should make other income streams — say, corporate earnings — relatively more valuable. A rise in interest rates makes bonds more attractive.

Friday, July 10th, 2026

Bill Bonner, from Youghal, Ireland

We left off reading the headlines and wondering...while we were were supposed to be watching the grandchildren...if the Primary Trend had stolen a march on us — and changed directions.

Oil slipped down. Gold sagged. Silver was cleaved in two. What is going on? A real change of course...or another head fake?

Let’s begin by recalling where we thought the Primary Trend was taking us. At the end of the last century the real price of US stocks, measured in gold, stood at an all-time high. It took 44 ounces of gold to buy the 30 Dow stocks. We mark that giddy point as not only the high water level for US stocks, but the zenith of the US empire, about equal to Trajan’s reign for the Romans or to the turn of the century — 1900 — for Great Britain.

The sun set on the British Empire in 1956. Then, the US took the role. For the US empire, the sun still shines. But it is weak, nostalgic and low-in-the-sky, more like October than June.

The Dow/Gold ratio went as low as 9 in February 2026...suggesting a loss of 75% of the stock market’s value. Since then, it bounced to a present value of 13. This is still less than a third of the high set in 1999.

But for the last four months the price of US stocks — in gold — has been creeping up (largely because gold has gone down in dollar terms). The question on the table, plain and simple, is whether this represents a fundamental sea change in the financial world...or just the regular chop and slop on the surface.

We never know for sure, of course. But at 9 times the price of gold, this past February, stocks weren’t cheap. We look for a level of 5 or lower before we mortgage the house and sell the family silver to go ‘all in’ on stocks.

Not that we know what direction the markets will take. We can’t predict the future. All we can do is await that outward sign of inner grace — a price so low that the risk is greatly reduced and the future can take care of itself.

Stocks can go up anytime. But a major shift in the Primary Trend only happens after they hit an historic low.

When will that happen?

Oh, c’mon, Dear Reader. You can’t expect us to know what is going to happen and WHEN it will happen, too. That’s asking too much.

All we know is that stocks were not historic bargains in February...and we want historic bargains before we make an historic shift in our investments. Currently, in dollar terms, stocks are at an historic high, not an historic low. And it’s a rare and lucky investor who makes money by buying at the top.

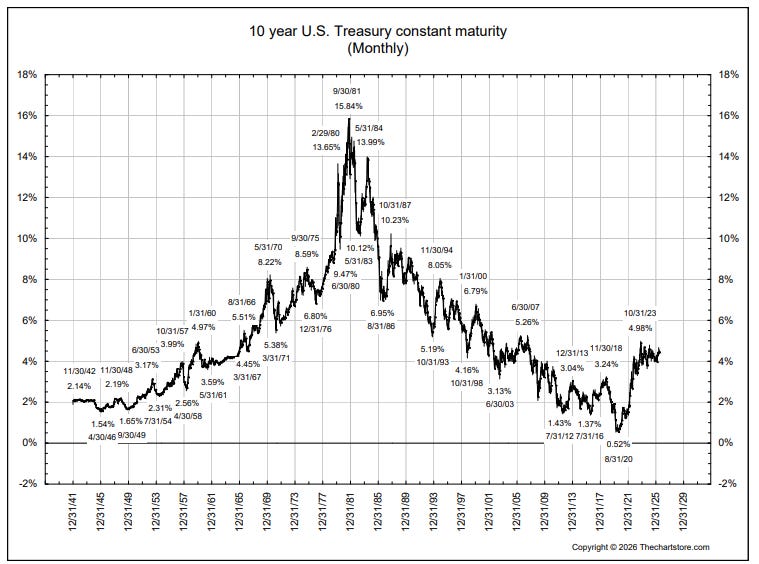

There’s also a Primary Trend in the credit market. It doesn’t coincide directly with the Primary Trend in equities. But the two are related. A sustained drop in interest rates should make other income streams — say, corporate earnings — relatively more valuable. A rise in interest rates, on the other hand, makes Treasury bonds, and other credit offerings, more attractive.

After Paul Volcker broke inflation’s back in the early ‘80s, stocks could enjoy two decades of jolly gains, gently coasting on declining yields. As interest rates went down, stock market earnings became inherently, mathematically more appealing...pushing up the Dow to the aforementioned 44 to 1 ratio with gold in 1999.

After 1999, interest rates continued to go down...and stocks continued, generally, to go up, but only in dollar terms. Not in terms of gold. And then, in July 2020, the long Primary Trend in the credit market stumbled, wheezed and finally came to an end. It had taken the yield on 10-year Treasury bonds from over 15% in 1981 to under 1% in 2020. Now, the yield is over 4%. And most likely, it will go much higher.

First, interest rate cycles are long. One generation learns (from borrowing too much money). The next forgets. The last entire cycle, from ultimate low to ultimate low, bottom to bottom, took 71 years, from a Post-WWII low to the high in 1981 and on to the final low 39 years later.

Another reason the Primary Trend in yields has probably not run its course is that yields are based on funny money, not gold. And the guardian of America’s funny money, the US government, will need to ‘print’ a lot more of it to keep up with its spending commitments. This will mean more inflation. And investors will need higher interest payments to make up for their losses of purchasing power.

And if interest rates continue to rise from here — though, perhaps with a deflationary interruption — stocks will be battered by competition from ‘risk free’ assets (US Treasury bonds)...and will most likely fall.

The fall may not be visible by the typical investor. Prices are quoted in the same funny money that the feds control and need to print. As in the 70s, we may see nominal prices holding steady...or even rising...as inflation reduces real values. Or, that crocodile we mentioned yesterday may finally sink its teeth into the stock market’s neck.

Remember, too, that buyers of US stocks and bonds come from all over the world. And they have their own problems and opportunities.

As Tom mentioned on Wednesday, China is growing its money supply even faster than the US. And the ‘Islamic Republic of Japan’ is now finally getting what it deserves from its own fake money-printing spree. Fortune:

The yen is quietly crashing as Japan’s debt crisis bleeds into currency markets, and efforts to halt the slide are doomed to fail, economist says

As foreigners grapple with their own crises, they may pull out of US debt and equity markets. Another reason the basic, long-term direction for America’s stocks and bonds is probably still down.

So, has the Primary Trend changed? Not likely. Look for higher interest rates and lower stock prices (measured in gold)...if not this year, maybe the next.

Regards,

Bill Bonner