Sky High

No situation is so grim... or so hopeless... that a determined leadership in Washington can’t make it worse. And since were looking for the ‘worst case’ scenarios, let’s look a little further.

Tuesday, November 19th, 2024

Bill Bonner, writing today from Baltimore, Maryland

Uh oh... here’s tech showboat, Cathie Wood:

The Reagan revolution extended through President Clinton’s administration, leading to lower taxes, stronger GDP growth, and a bull market rewarding active equity management that lasted nearly 20 years. We believe that this bull market has just begun to broaden out.

Morning in America? Better check the clock.

Donald Trump is in a tough spot. Because this economy today is in no way similar to the economy that greeted Ronald Reagan. It is almost the exact opposite — with a 4.5% Fed Funds rate…rather than the 20% rate that greeted the Gipper. And when Reagan looked at the feds’ books, he found $900 billion in debt. Today, there’s $36 trillion in debt, rising at $3+ billion per day.

As for asset prices, in 1980, they had been sinking since 1966, not rising 44 times in the last 44 years.

Reagan also had the benefit of a real inflation-fighter at the Fed — Paul Volcker, who could reduce interest rates as inflation cooled off. Lower rates meant higher asset prices. And as Volcker won the fight against inflation, the bond vigilantes could hang up their spurs. They weren’t needed.

But today, asset prices are already sky high and ready for a correction. And since the Great Boom ended, in July 2020, the Fed can no longer support the stock market without risking two unhappy consequences.

First, as we’ve seen since September, the bond vigilantes are back in the saddle. The Fed cuts short rates... and long rates rise. Investors know what time it is. They expect more inflation. Not only that... they seem to be doubting the good faith and full credit of the US government itself. Our Investment Director Tom Dyson comments:

US Treasury rates are the highest they've been in decades relative to everyone else's rates.

Not only are Treasury bond yields cheap relative to stocks, but they're cheap relative to corporate bonds, bonds from other countries, and commercial property cap rates.

In other words, it looks to me like Treasury bonds have lost value relative to the rest of the asset universe... stocks, foreign bonds, corporate bonds, junk bonds, property etc, etc...

Which implies investors are specifically marking down the creditworthiness of the federal government’s paper.

Second, higher long-term rates set in motion trends that are the opposite of the Reagan years. Instead of rising real asset values, we should see them fall. Instead of an economic boom, we should see a bust. And instead of financing small deficits at declining interest rates, the Trump team will be financing big ones at increasing real rates.

So, what’s new? No situation is so grim... or so hopeless... that a determined leadership in Washington can’t make it worse. And since were looking for the ‘worst case’ scenarios, let’s look a little further.

Prominent among the additional risks is the call for trade barriers. The US doesn’t just import stuff. It also exports stuff — $3.5 trillion worth each year. And it wouldn’t be at all surprising if the countries that suffer higher US tariffs, set up some tariffs of their own. This is what happened after misters Smoot and Hawley enacted a tariff bill in the US in 1930. Trade declined and much of the world went into a depression.

Trade is what keeps the world economy in business. Only very poor countries — who have nothing to export and no money to buy imports — don’t rely on trade for a substantial part of their GDP. The others need to buy and sell... and depend on it not only to meet their daily needs, but also to keep up with their debts.

The defining stupidity of the whole boom-bubble era, 1980 to 2024, was the role of interest rates. From double digits — 15% for a 10-year Treasury in 1981 — down to no digits at all. On August 3, 2020, the yield on a 10-year treasury note was not even a whole number... it was just a fraction of 1%.

Pushed down by central banks all over the world, the ultra-low lending rates led to an ultra-abundance of debt... now totaling more than $300 trillion.

Take away the $25 trillion in international trade... or even a small portion of it... and it becomes much harder to keep up with debt payments. Here’s Bloomberg with an analysis of Trump’s tariff proposals:

Of all the goods traded globally, 20% either go to the US or come from the US. In our model with tariffs, we’re looking at that falling to 9%.

We don’t have 100% confidence in these figures, but that looks like a loss to the US economy of about 10% of its GDP. And then…loans of all sorts go unpaid. Business profits shrink. Banks go bankrupt.

In short, in addition to the massive financial correction described above, we could have another worldwide depression... similar to what happened in the 1930s.

That is a worse case scenario. But it’s not the ‘worst case’ scenario. It wouldn’t be the end of the world, in other words.

But we’ll come to that tomorrow.

Regards,

Bill Bonner

Market Note, by Tom Dyson

What does it mean for investing when asset prices are so high that returns from corporate profits or commercial rents or even loans to US corporations are lower than the risk-free rate of return? Well, sir, either those assets are historically overvalued or that’s not a risk-free rate. I’ll have more to say about this in my report for paid subscribers tomorrow.

Source: Kenneth Miller Via X

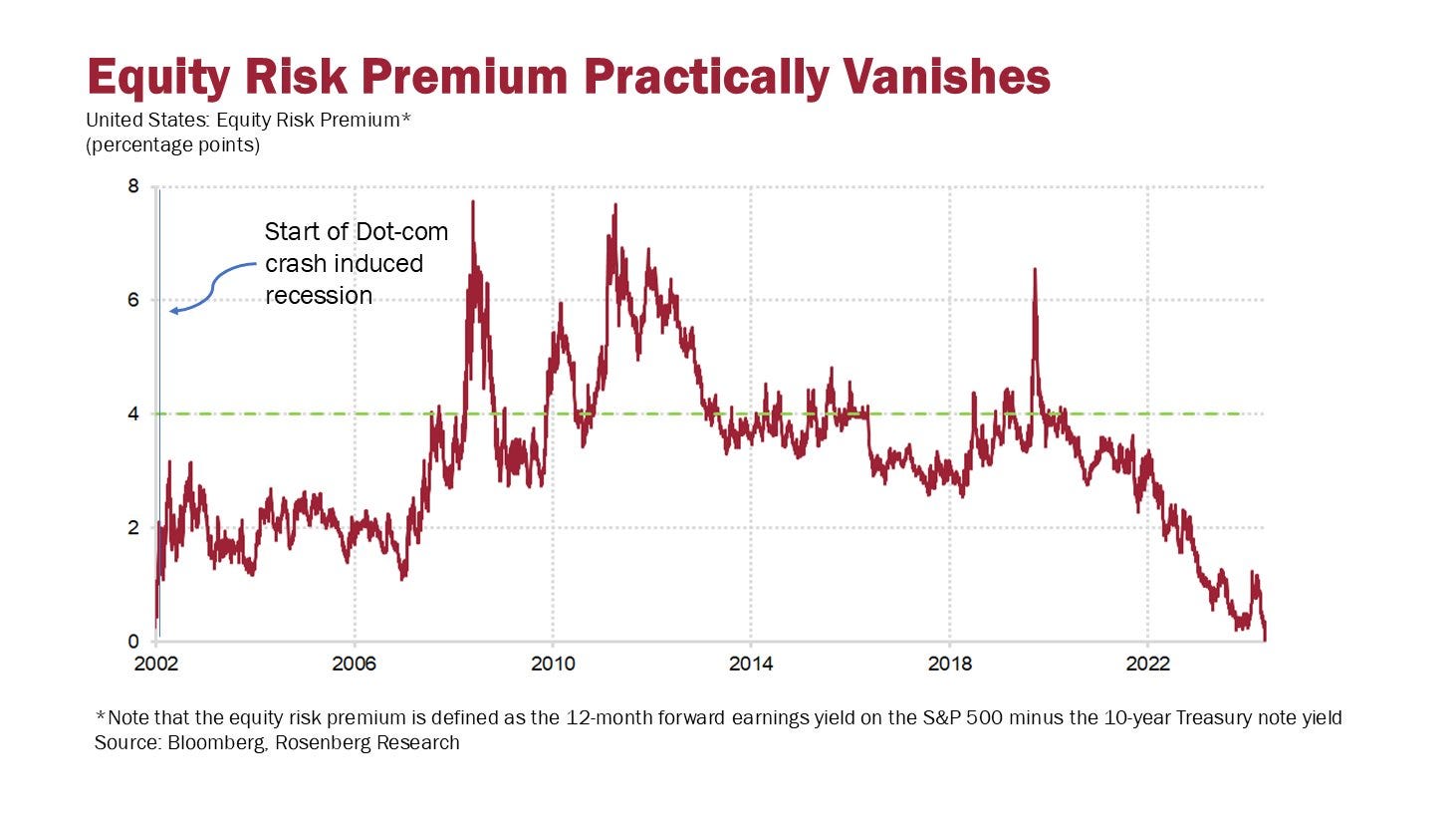

Source: David Rosenberg via X

Bill - once again you are spot-on! The euphoria that seems to now permeate the U.S. will be short lived. There is no place to run away or hide from the DEBT. And, amazingly, no one is talking about the debt - like it just doesn't exist. The good ol' USofA isn't little Argentina and Trump and Team aren't Millei. It is going to get UGLY sooner than ya'all think. Enjoy yourself until January 20th and then I would suggest you pull your head of out of your *** and smell the coffee. It is going to be a capital SUCK IT UP, BUTTERCUPS!

Bill, your tariff worst case scenario assumes all trading parties will be treated equally. That's not my understanding of how Trump plans to utilize tariffs. Yes, the tariffs will initially disrupt trade with the newly designated non-preferred partners. The slack will be picked up by the newly designated preferred partners along with the reshoring of manufacturing. Ask yourself this question: Can you have balanced trade when your partner/s utilize mercantilism? I think we all know the answer to that question and understand that perennial trade deficits are not sustainable. Just a little constructive criticism as I expect much more from you than the MSM talking heads.