Sunday, March 08th, 2026

Denver, Colorado

by Dan Denning

Bull markets become bear markets when liquidity matters more than valuations. It starts to matter more because there is less of it. First a little less. Then suddenly nowhere to be found.

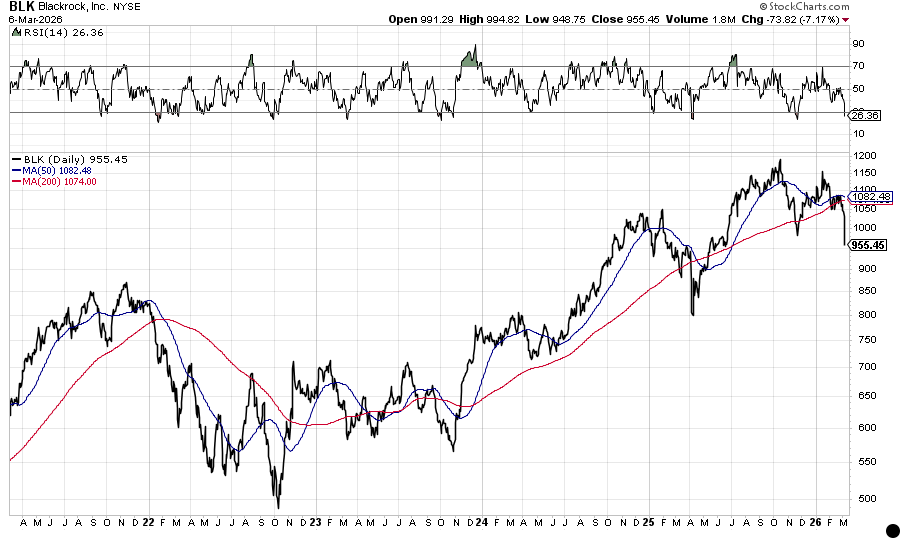

BlackRock is the world’s largest asset manager, with $14 trillion in assets under management. Blocking $1.2 billion in redemptions from one of its private credit funds isn’t a catastrophe. Not yet at least. But we’ve got our eyes on it.

BlackRock, Blue Owl, Blackstone…these are the names in private credit we’re starting to hear more about. These investments promise higher returns to high net worth investors. But the money is illiquid. So what comes next?

Credit events are like infectious diseases. They are bad enough for those that have them. But when they jump from one carrier to the next, from private markets to public markets, that’s when you get bigger problems.

If the liquidity disease moves from private credit to publicly listed asset managers…and then to banks…and then to insurance companies…well then valuations suddenly matter a lot…and mean reversion (a stock market crash) becomes a real risk in 2026.

But I’m sure it’s ‘contained.’ That’s what Ben Bernanke told us about subprime mortgages in 2007. And it’s not like panic is contagious in financial markets, is it?

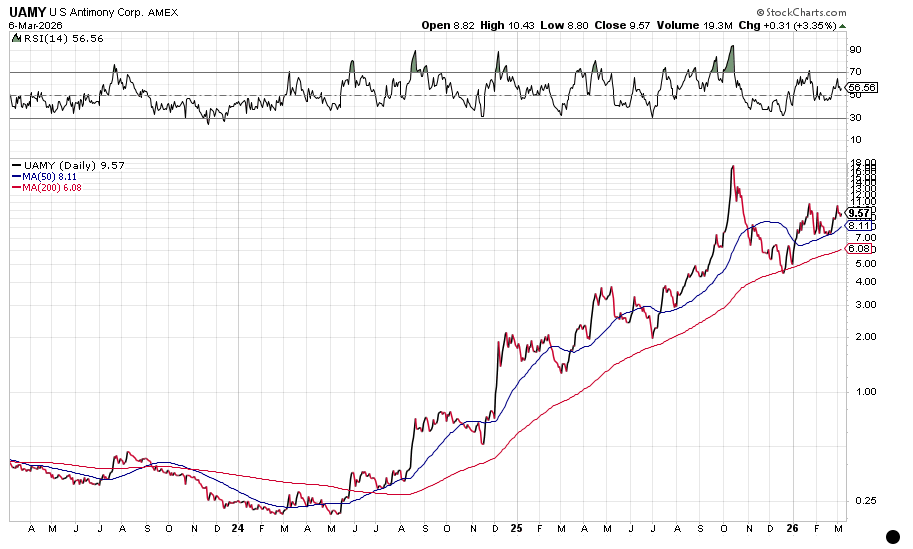

Meanwhile, the US war machine is hitting up the private sector to ramp up production of critical minerals and build out the domestic supply chain as quickly as possible. Uncle Sam’s Defense Industrial Base Consortium identified thirteen critical minerals and metals it wants US industry to…secure.

By ‘secure’ I mean, build out quickly a domestic supply chain for mining and processing these elements for the Pentagon. The critical minerals in question are: arsenic, bismuth, gadolinium, germanium, graphite, hafnium, nickel, samarium, tungsten, vanadium, ytterbium, yttrium and zirconium.

This is all part of ‘Project Vault’, the $12 billion plan to stockpile elements and metals the US depends on the rest of the world for (mostly China and Russia). The Department of War announced a $27 million investment in US Antimony Corporation [UAMY]. Among other things, antimony is alloyed with lead to make bullets harder. I first wrote about UAMY in PM Dawn, just before Christmas last year.

We’ll continue to track this trend at BPR. I may even ask Bill about having the government as an investment partner when I speak with him next week. We’ll be sitting down for our latest quarterly State of the World interview. If you have a question you’d like me to ask Bill, leave in the comments below or send it to bpr@bonnerprivateresearch.com

Until tomorrow,

Dan

P.S. The tariff news got buried by the Iran war last week. But the Congressional Budget Office quietly put out a note this weekend that the Supreme Court ruling would add $2 trillion in deficits over the next ten years ($1.6 trillion in ‘primary’ deficits and $400 billion in interest expense). The US dollar could not be reached for comment. Gold, being an inert metal, also had nothing to say but currently trades $5,181/oz.

BPR Week in Review

Dan, I would be very interested to year you and Bill comment on David Webb's book, The Great Taking. With the imminence of a revert to mean crash, Webb's well documented thesis is an exitential threat to much privately held (so-called) wealth. Many thanks!