Friday, March 13th, 2026

Laramie, Wyoming

By Dan Denning

The math is brutal. And inevitable. If you thought a trillion dollar deficit halfway through the government’s fiscal year was bad, you’re right. If you thought $40 trillion in debt (a 100% increase in the last ten years, from $19.2 trillion 2016) was a problem, you’re also right. But a problem when? And how? And as investors, what should we do about it?

The problem is now. And the threat is a continuation of the Primary Trend that began in 2020, higher interest rates for the next cycle; ‘cycle’ being loosely defined as this new era in money, interest rates, politics, military affairs, and the 21st century American Empire.

But what does all THAT mean?

The government assumes it will have to refinance around $30 trillion in maturing and new debt over the next ten years at an average interest rate of 4.2%. If rates are pushed higher by inflation, to say 5%, that’s $1.5 trillion in new interest expense on debt that needs to be refinanced and around $500 billion on new debt. Let’s call it $2 trillion–and remember that’s on TOP of the $1 trillion per year we’re paying now.

But wait!

Observe the chart below. In the last stagflationary cycle of the 1970s (the introduction of the credit collar, oil embargo, big move in gold prices) interest rates on the 10-year US Treasury note were well above 5%. They peaked above 15% (with the Fed funds target rate closer to 20%). Now here’s the scary math…

At an average 10-year yield of 10%, interest expense grows by $15 trillion over the next ten years. Around $11 trillion is the bill for refinancing debt that matures in the next ten years. Add in another $4 trillion on new debt issued to cover annual deficits of $2 trillion.

You see the problem. The solution, as Bill mentioned in our Private Briefing recorded yesterday, is not complicated. Cut federal spending back to 2019 levels. That would balance the budget with today’s revenues. Then slash defense spending, means test Social Security benefits, and end the foreign wars. Put America and Americans first and return to sound money (which might require higher interest rates if you are to find buyers of your debt in the free market rather than having the Fed print up the money to finance the Warfare/Welfare state).

No one in Washington, except Congressman Thomas Massie and Senator Rand Paul (both from Kentucky) seem willing to vote for anything that would prevent the looming fiscal disaster from destroying American standards of living and quality of life. So we will have to fend for ourselves, not wait on public policy or politicians, stay in Maximum Safety Mode, and try to take it year by year. Speaking of which…

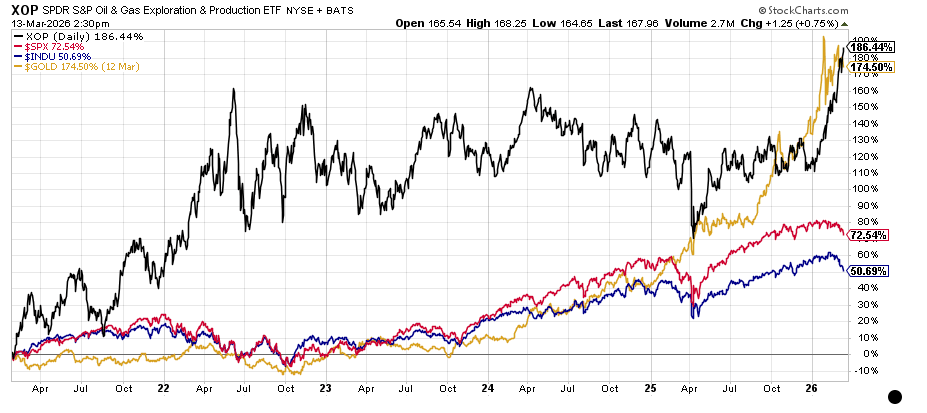

Bill and I covered a lot of ground in his latest quarterly State of the World briefing. I’m having the video transcribed now and will publish it for you tomorrow. One thing we did NOT cover was the status of our current Trade of the Decade. Bill asked about that this morning via email and I sent him the chart you see above.

This covers the performance of XOP since we added it to the Official List in January of 2021. Gold and oil up, blue chips down. That’s it in a nutshell. And if you missed Tom’s update on Wednesday (Runaway Train), here was a key observation:

‘Oil is to the real economy as credit is to the banking system. When it dries up, everything grinds to a halt. The difference, of course, is the Feds can’t print their way out of an oil crunch, so it’ll be much harder for them to intervene.’

At the end of January, the gold/oil ratio was 83 (an ounce of gold divided by the price of a barrel of West Texas Intermediate crude oil). Except for April of 2020, when oil briefly went negative and the ratio spiked to 132, oil has seldom been cheaper in gold terms.

Or HAD been. That’s changing now. That is why Tom added oil and gas investments to the Official List.

I asked Bill if he recalled any ‘lag’ between the spike in oil prices in the 1970s and higher prices for everything else in the economy (gasoline and jet fuel obviously went up first). That’s the big question now: How quickly will a ‘closed’ Strait of Hormuz translate into higher inflation for producers AND consumers all over the world, and especially right here in the US of A?

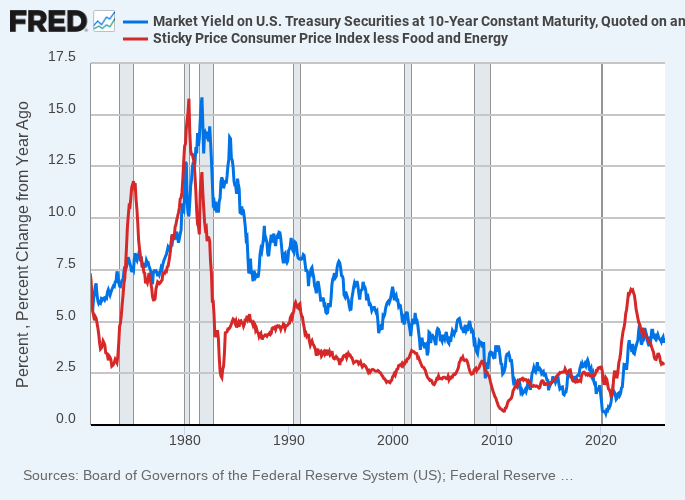

The red line on the Fed chart above shows a second wave in the ‘sticky’ inflation measure tracked by the US central bank. Inflation AND inflation expectations went higher and stayed there. Higher inflation required higher nominal interest rates, something the US government simply cannot afford today (the debt-to-GDP ratio was 30% in 1974…it is 120% today).

What next?

The war with Iran could end quickly. It is in no one’s interests for the Strait to remain closed. The shock would trigger a global depression. But if the conflict drags on and the spice no longer flows, then inflation will be impossible to avoid. That may already be the case. The Treasury Secretary can try and manage the oil price lower through the futures markets. But at the end of the day, either the oil is flowing or it is not.

By the way, threatening to close the Strait was not an effective deterrent against a US attack on Iran’s nuclear program. But now that the genie is out of the bottle and the Strait is actually closed, it may prevent things from escalating further. Or not. We’ll see soon enough. In the meantime…

I’m on the lookout for signs that stress in the private credit market (gates and halted redemptions in funds with exposure to pre-public software companies) is leaking over into public markets and other assets. The issue, crudely simplified, is that if AI agents render the trillions in private investment in software companies…bad…well then this asset class is in trouble.

This would not be surprising. The kinds of ‘income’ promised by private credit funds are typical of late stage credit bubbles. Publicly listed stocks become over-valued. To sell more product, new vehicles are created to attract high net-worth speculative capital. The companies invested in often have no revenue–meaning the sky is the limit and valuations are irrelevant.

There is one big issue that comes up for anyone NOT involved in the private credit market. Investors who are panicked from losses in private markets sell publicly listed stocks, gold, and Treasury bonds–basically anything liquid that can cover losses. This leads to margin calls and more forced selling (margin lending is at a record $1.2 trillion and 6% of GDP, compared to 2.5% in 2000).

In other words, the blowing up of a bubble in a small, peripheral market in which you’re not invested is exactly the thing that can bring about a cascade of selling. It can also engineer a change in investor psychology, from greed to fear. And then to panic.

But I’m sure everything is contained and a blow up in private credit markets would never be the pin to prick the equity market bubble. Absolutely impossible. Called Ben Bernanke to double check. Confirmed. Move along. Nothing to see here.

HYG has rolled over. But it’s not in free fall yet.

Until next week,

Dan

P.S. Want to know what omniscient surveillance combined with AI targeting might look like? Check out this video. It shows the Maven integrated surveillance platform in action. Add Anthropic’s Claude to this and you get a rapid-fire analysis and targeting system for 21st century AI-drove-pre-emptive American warfare on a global scale.

As the cost of making war goes down, the frequency of violence goes up. That’s how it would normally work. But the way we measure both the ‘cost’ and the ‘returns’ on modern warfare are up in the air. AI tools may make war planning and intervention seem faster and foolproof and bloodless. But how did anyone at the Pentagon not foresee or measure the cost of Iran closing off a key oil choke-point?

It’s almost unfathomable that somewhere in the Pentagon’s thousands of pages of war plans, there isn’t a chapter or two dedicated to the worst case scenario in the Straight of Hormuz. But maybe technology has seduced our war planners and politicians into believing that wars can be fought and won in the same time it takes the average American to binge watch a streaming series on Netflix.

This is war as ‘workflow.’ And it’s extremely dangerous, especially with the chance that AIs could have autonomous ‘kill decision’ authority, or give themselves that authority without human permission. And let’s not forget that real human beings are put in harms way delivering weapons, fuel, and supplies, not to mention the people on the receiving end of our bombs. We also assume these powerful surveillance, targeting, and predictive algorithms would only be used against malicious foreign enemies and non-state actors.

But once the operational concept has been ‘proven’ and deemed successful, what is to prevent it from being used here in America against Americans? What kind of Americans? At first, it would be used to identify and prevent the kinds of shootings we’ve seen across the country this week. But later, against everyone. All the time. what then?

P.P.S. A lot HAS been happening with AI agents and the Pentagon. Stories on X quoted from a slide deck in which the Pentagon is soliciting Wall Street for traders to come and join the Pentagon’s Economic Defense Unit. The short version is the Department of War is looking for a team of 30 Wall Street analysts to invest $200 billion over three years.

The mission is to help ‘deter our largest adversary from gaining military superiority,’ to ‘reshore US manufacturing’ and secure ‘a better long-term future for Americans.’ This seems different from In-Q-Tel, the non-profit firm chartered by the CIA (officially) in 1999 to make venture capital investments in promising Silicon Valley technology firms.

This is more industrial. It’s a vast expansion on Project Vault, which seems more like a quick ‘sprint’ to fast-track critical mineral investment production and refining in the US (and shore up domestic supply chains) by making investments in publicly traded companies. From the slide deck, the new EDU will focus on six areas:

Industrials (manufacturing, supply chain security, bulk materials, munitions, drones)

Technology (warfighter enablement, dual-use tech, R&D)

Telecommunications (undersea cables, satellites and space, spectrum and Future-g)

Energy (generation, transmission, distribution, storage and battery technology)

Global logistics (strategic maritime, logistics infrastructure, aerospace, heavy logistics)

Metals and mining (exploration and extraction, processing, refining, conversion, end use)

Lots to unpack here. Are these the actions of a government already preparing for the next war (with China) before its finished the current war with Iran? It’s certainly a departure from fifty years of industrial and trade policy which favored Wall Street, the dollar (as a global weapon), and finance over manufacturing, industry, and trade. Will anyone on Wall Street do their patriotic duty and move to DC to join the team?

In the spirit of the age, I asked Claude (Anthropic’s AI) to act like a venture capitalist and build a portfolio of companies that might be in the cross-hairs of the EDU. I added a caveat that there should be ten large-cap ‘safe’ companies and then up to twenty hyper speculative or risky companies. I then checked for ‘hallucinations’ and accuracy with Perplexity (to make sure all these companies actually exist and all the news flow is accurately reported).

Please note that this is not investment advice and none of these positions are on the Official List.

As the Research Director, I’m sharing some of my raw research with you, using new (and untested) AI tools. There is a LOT more research to be done…and it’s not clear Pentagon investment in any of these companies (big or small) will move the needle on the stock price (some of the stocks are already expensive to begin with).

But if the US now has an industrial policy, and it resembles capitalism with late Soviet characteristics, then it’s a theme worth exploring. It could be that this marks a rejection of the post-Bretton Woods era of the credit dollar as the chief pillar of national security.

It could be that we’re returning to an FDR-style, top-down, wartime industrial policy where the government invests and intervenes (or even nationalizes) industries it deems critical to national security. If you’d like me to explore this subject further, leave a comment below.