Friday, July 03rd, 2026

Laramie, Wyoming

By Dan Denning

Happy 250th America!

🎆 🎇 🧨💣🇺🇲

And here’s to all those who celebrate liberty and the idea of America. Fire up the barbecue. Crack open a beer. Light up a sparkler.

Enjoy!

But don’t think any of the festivities this weekend will keep the coming reckoning at bay. Not gonna happen. In this week’s research note, I’ve compiled more evidence. But not just about valuations. Also about certain indicators that will help us narrow down the ‘when’.

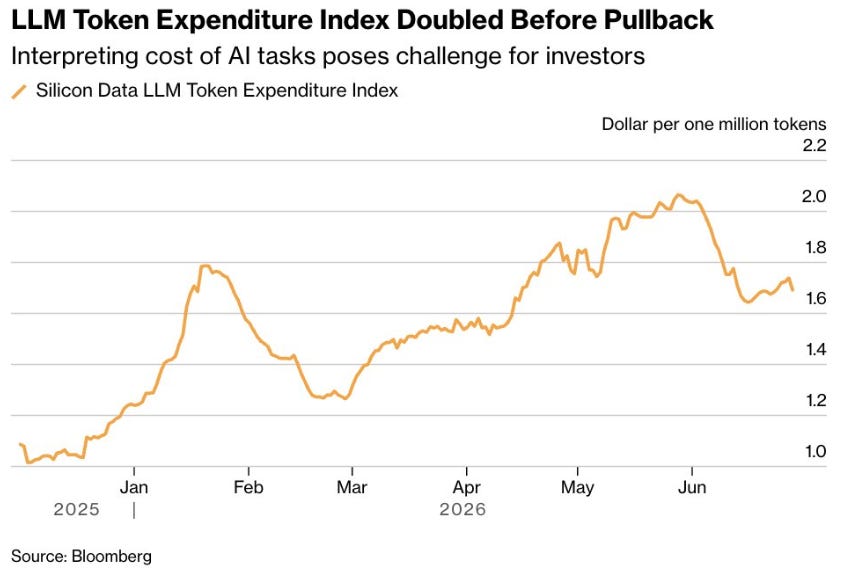

Before I get into them, check out the chart above. It’s an index that measures both the price and the volume of AI use by big businesses. At the ‘enterprise’ level, big businesses have been spending heaps of time and money trying to make AI (subscription-based Large Language Models like ChatGPT or Anthropic’s Claude) do something.

C’mon AI! Do something! Anything, really.

Replace lawyers and accountants, pad the bottom line, automate and optimize processes…be the transformative general purpose technology Silicon Valley has told us you’ll be.

But what if it isn’t?

There are several good reasons why ‘token maxing’--spending millions on AI compute blindly–might be in a downtrend. First is that the US players are closed-source, subscription-based models. You can’t customize the model. You don’t really own it. And there’s no guarantee the proprietary intellectual property from your business that you entrust to the AI vendor is secure…or won’t be used to copy your business model.

Second, the open-source models from China are cheaper and by most accounts, just as good. Granted, the Chinese open-source models may have also…effectively borrowed all the training data used by US companies. But the US companies ‘scraped’ a lot of the data they used to train their model and didn’t pay for it either. My point is that neither group is in command of the moral high ground here.

The third reason for the decline in AI spend is that customers may have doubts about whether they’re getting–or will continue to get–the best services (at any price). I’m referring to the Trump Administration’s brief suspension of Claude’s Fable model on national security grounds last week. It now appears that new models will require Uncle Sam’s permission to go public…and the implied threat of nationalization (in which case the government owns third party data) is now a factor users must consider.

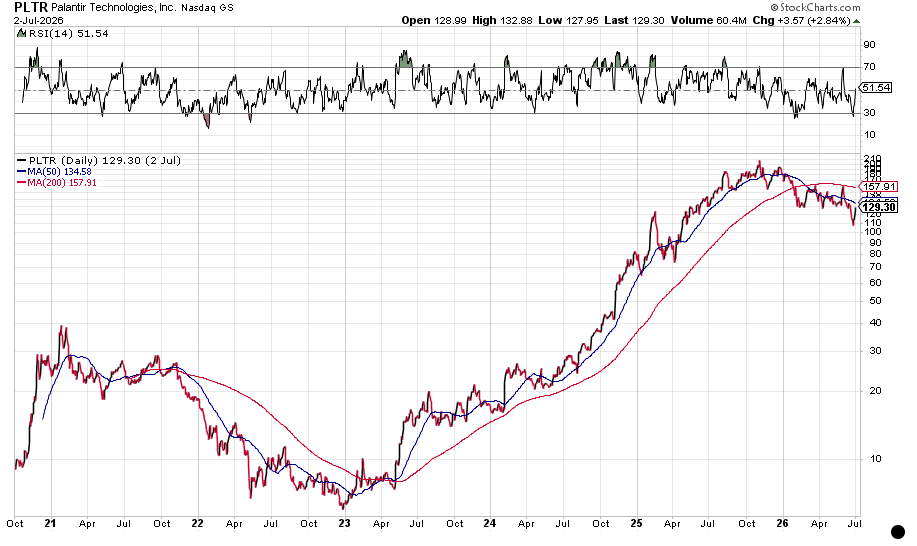

I also refer you to Palantir’s stock chart above. And I encourage you to think about the term ‘AI Sovereignty’ this weekend. The ‘frontier’ companies in AI like Anthropic and OpenAI have basically built a brain you can rent. But they don’t show you how they trained the brain (is it Woke…is it anti-racist…does it have ‘guardrails’ to prevent you from ‘wrong-think’?) and they don’t let you customize it. You pay to use it…in the way they allow you to use it.

Palantir’s CEO Alex Karp made waves this week when he all but said that LLMs and AI based on the subscription model aren’t going to make it. He implied these companies have no real business model going forward. Why? Corporations and nations want to ‘own’ the whole technology and keep their data private and proprietary. That’s not what the big US firms offer.

Karp is partly talking his own book. Nvidia has an ‘open weight’ model called Nemotron. It runs on Nvidia hardware. And you can run Palantir’s various software offerings on it. But you can tweak and improve the model to suit your needs (that’s partly what ‘open weight’ means)–without surrendering your data back to a model provider.

You get AI Sovereignty, in other words. That’s a world where you can run your own AI or army of agents on your own machines with no constraints. The individual, the corporation, and the government are all sovereign. Not the AI provider. Nemotron is also ‘multi-modal,’ meaning you can input text, images, video, and audio into your training data for the model. That’s a LOT more data for the model to ‘learn’ form.

Bottom line: If big corporate spenders move away from the ‘closed source’ frontier AI models, then it’s a danger to the hyperscalers, to the AI capex boom, and to the entire AI bubble that’s been building in the stock market since November of 2022. That’s what’s at stake. The catalyst for the Big Loss and the mean reverting crash.

Palantir’s stock chart doesn’t give any clues. It’s not an AI play. And you could argue that Palantir has been quietly delivering advanced business intelligence and analytics for the government (especially the Depart of War and intelligence services) for years. Maybe LLMs like ChatGPT are just the watered down versions of this technology that are ‘safe’ to make available to the public (on a subscription basis only…and if that turns out NOT to be a viable business model…than nationalization as an ‘intelligence utility.’)

Lots to consider. In the meantime, Fable is back, baby. It got out of Trump jail mid-week. And I put it right to work improving our BPR valuation dashboard. I’ve broken it up into three parts–Valuations, Triggers, and the Verdict. I’ll show them to you now…and I invite your feedback in making them even more useful. Let’s start at the beginning with valuations.

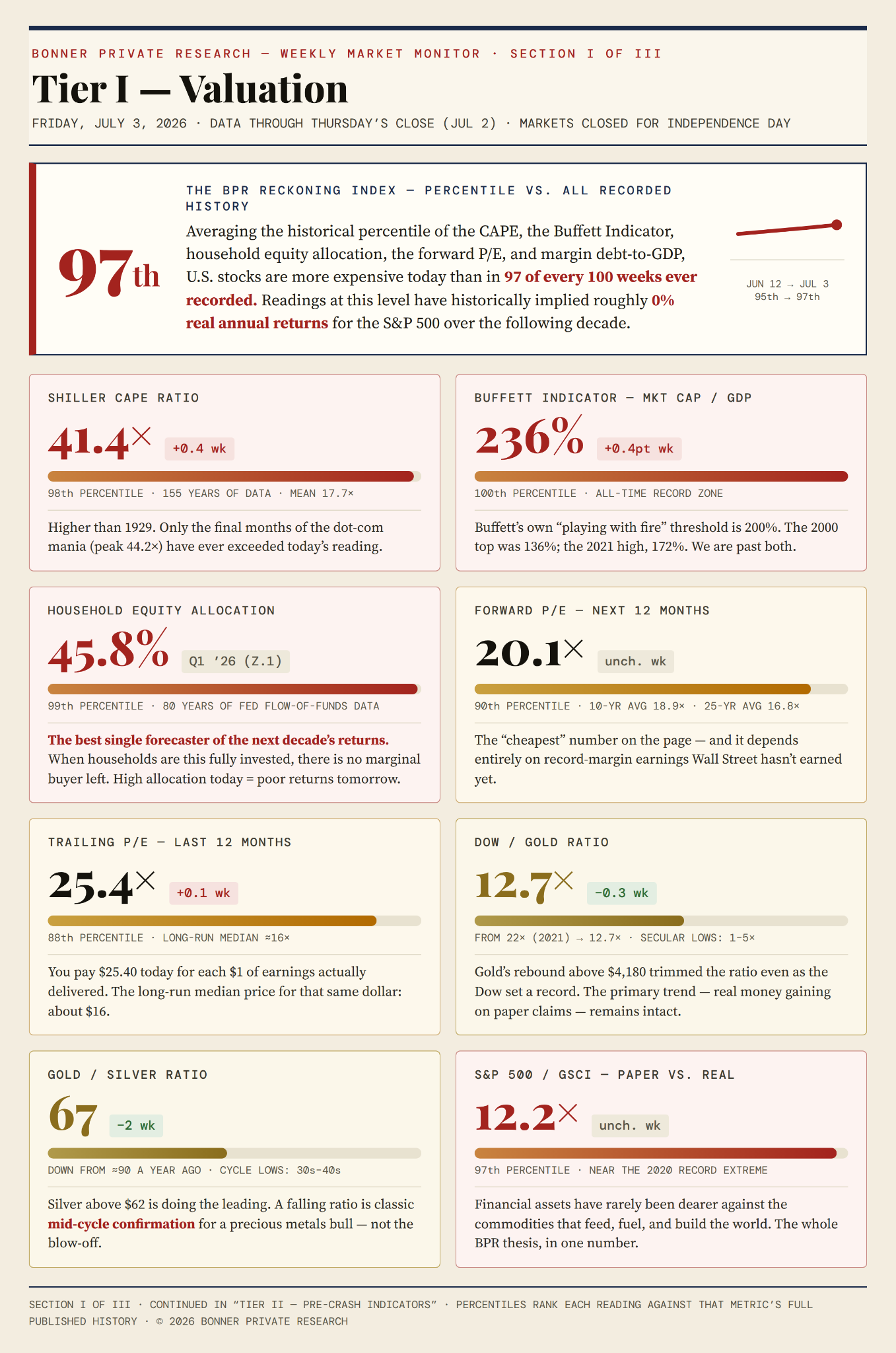

All honest measures of value — the CAPE, the Buffett Indicator, the price you pay for a dollar of earnings — will tell you the same thing today: U.S. stocks are historically expensive. That’s a fact.

But it answers only one of the two questions a serious investor needs answered. Valuation tells you the size of the eventual reckoning (how far we have deviated from historical levels). It tells you almost nothing about the timing (which I’ll come back to in a moment).

For example, Robert Shiller’s Cyclically Adjusted Price Earnings ratio (CAPE) CAPE is good at predicting ten-year returns but not especially helpful for what will happen in the next ten months. For the new and improved dashboard, we’ve taken out the silver/oil ratio and the equity risk premium. Both are too abstract with too little useful informational content. We may come back to them from time to time when relevant. But not each month.

We’ve replaced those two with three new ones: the household equity allocation, the gold/silver ratio, and the S&P 500/GSCI ratio. These are all additional insights based on financial data. For example, the household equity allocation is based on eighty years of Federal Reserve data. It’s a great forecaster of ten-year returns. At 45.8%, US households have a record amount of their financial assets in stocks. They are ‘all in.’

The gold/silver ratio is more controversial subject to debate about its value. It doesn’t tell you anything about the individual prospects for gold or silver individuall. But in my view, it does tell you roughly where we are in the precious metals bull market. The lower the ratio the later it is (silver rallies to catch up with gold). If this were a baseball game, I’d say we were in the seventh inning.

The last new valuation edition is the S&P 500 to Goldman Sachs Commodity Index ratio. In some ways, this is similar to the Dow/Gold ratio. But it’s broader. You can think of it as the ratio between financial assets and real assets, or ‘paper’ and ‘stuff.’

One last thing: we’ve added a percentile bar. This shows you where the current reading sits for as far back as the data is available. For example, there are 675 readings on the Buffet Indicator (market cap-to-GDP) going back over 56 years. This month’s reading is the highest ever (100th percentile).

The percentile shows you where today’s reading is relative to all past available readings. It doesn’t have anything to do with ‘fair value’ or ‘intrinsic value.’ Stocks could go higher. The bubble could get bigger. The experiment may run longer. Or it could blow up.

When you condense all our percentile indicators into ONE indicator–the BPR Reckoning Index–you get a more precise read of what all of them are telling you. And THAT tells you what you can likely expect from stock market returns for the next ten years. Now for the second part.