The Price of Glory

The founders, insiders, and anyone who already owns stock in these companies can’t wait for you to fill up your pension and 401(k) with shares. You are the liquidity they need to exit with a fortune.

Friday, May 22nd, 2026

Laramie, Wyoming

By Dan Denning

Well, how now, Dow? The big blue-chip index made a record intra-day AND closing high today. It went into the Memorial Day weekend strong, with a close at 50,579.

But wait!

In gold terms, the Dow is at 11.2. That’s higher than in the last few months. But it’s a long way off from the lows we expect it to make (under five, if past cycles are any indication). Below, we’ll look at broad money supply trends and total dollar-denominated liabilities in the global system…and what they mean for gold.

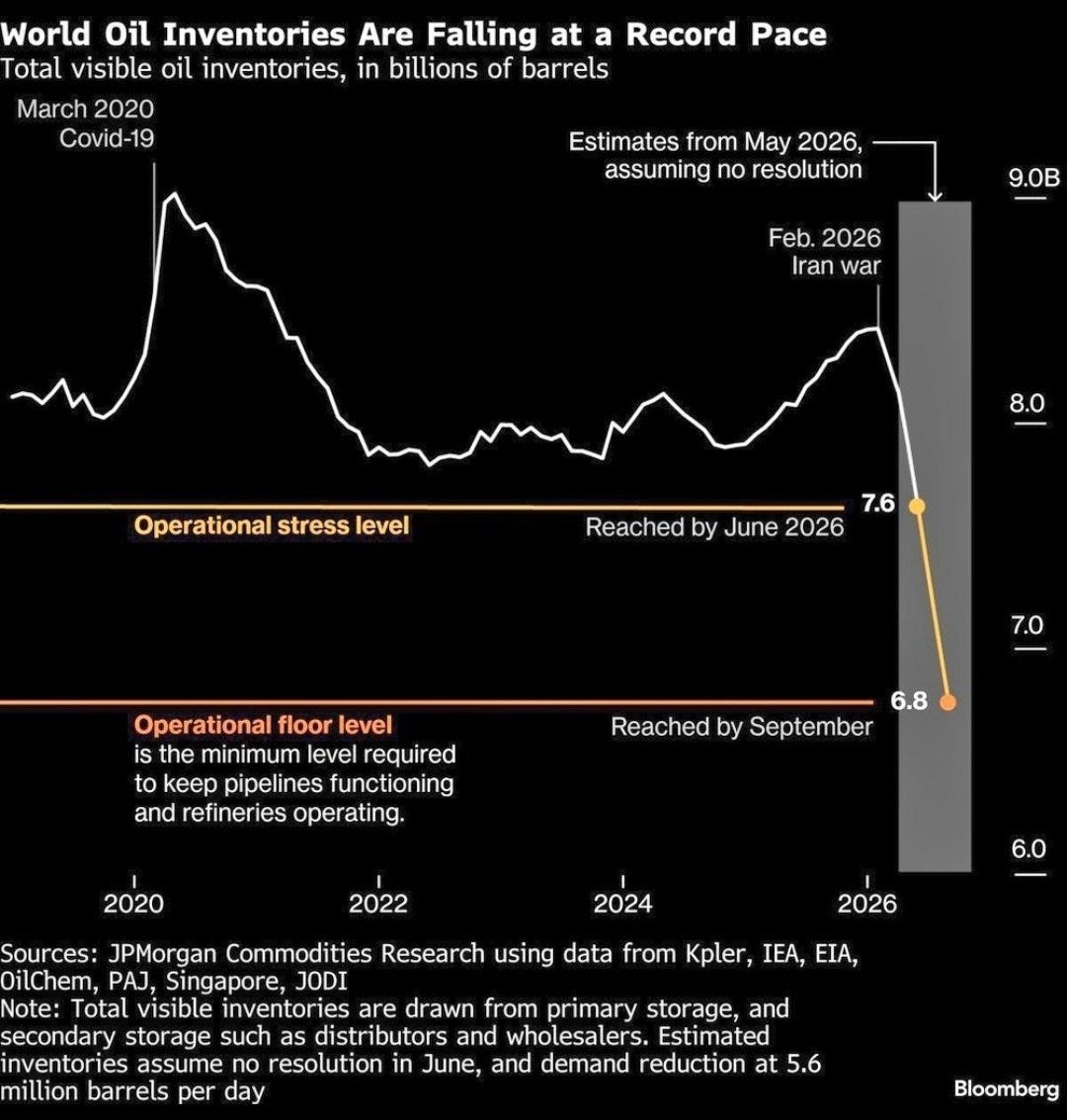

But first, late last month we said the clock was ticking on two things. First, the 90-day deadline on military operations in Iran. After 90 days, the President has to seek permission from Congress, or Congress has to explicitly authorize the operation. Second, Iran is running out of room to store the oil it pumps. Let’s begin with a chart.

What on earth is really happening in the oil market? The physical market is still pricing scarcity. The financial market is pricing a quick and peaceful resolution to the war in Iran. In fact, even though prices are still up from early February, the financial markets are acting as if the war is already over.

Which one is right?

Industry sources still quote a large premium for oil being offloaded from tankers in Asia. That is, the price at the port is higher than the price in the newspaper. The premium is smaller than it was a month ago. But it’s still there. (Many of the prices and data are behind industry paywalls or only updated intermittently, so the market is a bit opaque.)

Meanwhile, there is growing concern among energy analysts that the draw-down in commercial oil inventories will mean much higher energy prices this summer. There is an important distinction to be made between commercial oil inventories and strategic petroleum reserves held by national governments. The commercial inventories are stocks that are constantly drawn on. What’s the issue?

About a billion barrels of global oil supply have been “lost” due to the Iran war. It comes out to about 14 million barrels per day (bpd) after you subtract overland pipeline supply that’s still flowing from the 20 million barrels per day that used to transit the Strait.

Some releases of strategic petroleum reserves have offset that lost production. Higher prices have destroyed demand for oil in markets that can’t afford it. (There is even an argument to be made that global inventories may actually be rising…but I won’t get into that today.) And with financial markets expecting the current ceasefire to be permanent, the financial price of oil is lower than you might expect for what’s been called the biggest oil shock in history.

Oil analysts concede that the Iran war began with about 8.2 billion barrels of oil reserves around the globe (in commercial or other storage). That’s about 86 days’ worth of oil at current global daily demand of 95 mb/d. And that’s if all we had to live off of was the oil in storage — an unlikely scenario, as plenty of oil and gas are being supplied daily all over the world.

But here’s the big thing: all that oil in storage is not readily available. Some of it is required to keep systems pressurized and/or maintain critical supplies as defined by national security legislation. There is also a minimum level of reserves required to keep pipelines and refineries functioning normally. It is not available to be ‘released’ and make up for production interruptions.

Just where that level is — and how quickly we’d get there if the Strait doesn’t open and the war doesn’t end — is the big question. In the best-case scenario, the ceasefire becomes a formal agreement for ending the war. Oil resumes flowing through the Strait, although it’s not likely to happen as easily as flicking on a light switch.

If this happens, then you’d expect the oil price to come down even further. This has no effect on our long-term position in XOP, the oil and gas producers ETF we’re using to execute the Trade of the Decade. If anything, an oil correction might allow new readers to enter the position when the RSI is at or below 30. (We’ll let you know if that happens.)