The Gates of Vienna

The US is entering a debt crisis of its own making with the prospect of a wider war with Russia. But if the next President saddles up a War Horse, the move in gold could be higher than we expect.

Bonner Private Research

Friday, September 13th, 2024

Laramie, Wyoming

The painting above is Polish King Jan Sobieski outside the gates of Vienna on September 12th, 1683. Sobieski and his three thousand winged hussars broke the lines of the Ottoman Turks in a victory which European historians consider the beginning of the end of the Ottoman Empire (Vienna was as far as the Turks ever got into Europe). The battle began the day before, on September 11th, and there’s some speculation that Al Qaeda picked 9/11 for its attack on the World Trade Center because of this historical setback for the Ottomans (one it hoped to avenge and reverse by attacking iconic symbols of American power).

What the picture above doesn’t show you is how many people pushed and jostled me while I was trying to take it. Hardly anyone stopped to look because hardly anyone knows what it commemorates. I only knew it was there because my faculty advisor in college was Professor Francis Zapatka, a Jesuit-trained literature Professor with Polish roots who told the story more than once.

It’s hard to miss though. The painting is actually the largest painting on canvas in the entire Vatican Museum. I’d seen it once before, in college, when I spent a semester studying in Rome. I came back in the spring of 2018 for a vacation, where I had more time (and money) to enjoy everything Rome has to offer lovers of history, art, and architecture.

Even for the Eternal City, a lot has changed since the mid 1990s in Rome. Like all the beautiful places in the world, the Vatican Museum is crowded these days. Most people rush by the Sobieski painting on their way to the Raphael Rooms with no idea that an important turn in the historical tide of history is depicted right in front of them, larger than life. But I stopped to take a picture to remind myself that there are some periods in history–even particular days–where everything changes.

Political Risk

You’ll read a bit more about the Ottoman Empire in the Private Briefing I’ll publish on Sunday. Our latest guest was none other than the great Doug Casey. Doug’s spending the summer in Virginia and was kind enough to take an hour out of his schedule to talk about the state of the world (or the absolute state of chaos).

We talked about 9/11, famous (and infamous) Empires in history which the United States currently resembles, and what to expect from financial markets as the US election approaches. If you know Doug or have ever seen or heard him speak, you know he doesn’t hold back. It wouldn’t be a Casey conversation without a little controversy.

I was most interested in what Doug sees as practical solutions to our political problems. From Doug’s point of view, political risk is THE clear and present danger right now. For Americans in particular, our politicians seem hell-bent on leading us into a wider war with Russia (something Putin warned about this week).

Meanwhile, the gold market is telling Fed Chair Jerome Powell and Treasury Secretary Janet Yellen that the ultimate casualties of their feckless policies will be the US dollar and US government bonds. We may be watching the biggest de facto dollar devaluation in decades. Let’s examine the ugly guts with the graphic below.

US fiscal arrangements are falling apart rapidly now. The government deficit for the month of August was $380 billion, according to the Monthly Statement of the US Treasury. The entire national debt was $389 billion at the end of 1970, just before Richard Nixon replaced the Gold Dollar with the Credit Dollar.

There’s one more month left in the government’s fiscal year. By then, the total deficit for the year will be close to $2 trillion. When you dial back from the monthly level, you’ll find that net interest expense for the year is $843 billion. Total spending on war and armaments (defense spending is what the government calls it) is $798 billion. It already costs us more to pay previous creditors than to pay our soldiers, Marines, airmen, and space warriors.

Here’s the most alarming part: The TOTAL interest figure, year-to-date, is already over $1 trillion. It’s buried in the fine print. The ‘gross’ interest expense, which includes interest payments to government agencies that own Treasury bonds, bills, and notes, went over $1 trillion in August. That’s the first time that’s ever happened. The debt default train has left the station.

Gold usually trades lower on a Friday. Nobody knows why (although traders in the paper gold market seem to have a habit of hammering it down.) But we’re looking at a three per cent gain for the week and a close of about $2,600 for the first time ever ($2,602.20/ounce to be exact). Why?

US deficits are out of control. Neither candidate for President meaningfully addressed what they’d do to avert the coming dollar crisis. And despite all that, the market expects the Federal Reserve’s Open Market Committee to cut interest rates by either 25 or 50 basis points when it meets next Wednesday (even with core and ‘supercore’ inflation above the Fed’s target).

Precious metals are breaking out as fiat money breaks down. That’s what I noted when I looked at the table above from goldprice.org. Note that gold is up over 20% in ALL major currencies year-to-date. That didn’t even happen in the last big run up of 2010 (gold in Swiss francs was the laggard in 2010). With today’s close, gold is up 24.5% year-to-date in US dollar terms.

Fiat money (inflation via the printing press) goes hand in hand with the Warfare State. Not to beat a dead horse, but perpetual war requires perpetual debt. Central banks fund the war machine. The US would be entering a debt crisis of its own making with the prospect of a wider war with Russia (or Iran, or China). But if the next President saddles up a War Horse, the move in gold (in all currencies) could be even higher than we expect. How high?

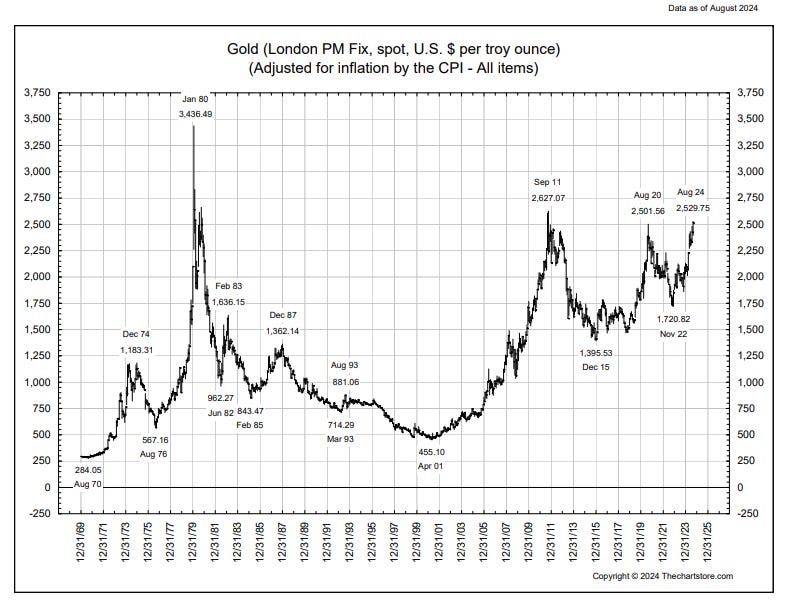

Just a reminder that we haven’t hit an inflation-adjusted all-time for gold yet. That’s still about $1,000 a way, based on the January, 1980 gold price in the chart above from Ron Griess at thechartstore.com. As Tom pointed out earlier this year, the recent triple top in gold is a line of resistance that will become a line of support. Once that line is broken, it would not surprise me to see gold move up in $100 increments on a daily basis (not without a lot of volatility, mind you).

Another factor, which I won’t get into in detail this week, is the maturity profile of US Debt. There is a line of criticism in markets that Treasury Secretary Janet Yellen has tried to influence this November’s election outcome by issuing more short-term government debt this year (Treasury bills rather than Notes or Bonds). We’re talking around $2 trillion in Treasury bill issuance, so it’s no small figure. Yellen has been suppressing concern about a US debt crisis.

Two things. By definition (and duration), T-bills (three months, six months, nine months) mature faster than Notes or Bonds. That means Janet has to roll them over, or refinance them, faster and more often. And when rates are rising, it means interest costs go up even faster as the previously issued Bills mature. The last thing America needs is a higher monthly interest expense on the national debt. But Yellen has virtually guaranteed that’s what we’ll see…but after November…when all the ballots are harvested and all the votes are counted.

The second thing is that Yellen has done her best to hide Washington’s fiscal train wreck from financial markets. Had she auctioned longer-term notes or bonds, the market (via the bond vigilantes) would have set the required interest rate to buy that debt. It’s unlikely that any of those auctions would have failed. But if demand for longer-term debt was lower than expected, or required higher yields to entice buyers, it would have been impossible to ignore the signal that US government debt is no longer ‘risk free’ or ‘safe’.

Judging by the gold price action, the markets are now fully aware that the US debt crisis is entering a new stage. It is both a dollar crisis AND a bond market crisis. But as Doug has famously pointed out, with every crisis, comes opportunity.

On the precious metals side, we’re already well-positioned for the move. On the bond or equity side, please note the chart above. IEF is an exchange traded fund that tracks 7-10 year US Treasury prices. There’s been a bit of a bull market in IEF since late October 2023. It was not the sort of thing we’d bother trying to trade (too little upside, too much risk, and we’re not traders).

But now, please note the Relative Strength Index (RSI) on IEF is at 70. That traditionally means it's over-bought and due for a correction. And IEF itself is trading at the same level as it was in the summer of 2022. It’s either different this time, or it isn’t.

You COULD make the argument that if the Fed is about to enter a rate cutting cycle (recession, higher unemployment) that would be good for bond prices (and that US bonds still get a reflexive ‘flight to safety’ bid during a geopolitical crisis). But I’m not going to make that argument. And here’s why…

First, as the old saying goes, if it’s in the news it’s in the price. This Fed rate cut has been widely telegraphed for weeks. That’s why IEF is ALREADY trading so far above its 100-day and 200-day moving averages. Buy the rumor, sell the news etc.

Second is the point Doug made in our Private Briefing. In this latest stage of the ongoing crisis, the major political risk resides in Washington, not Moscow, Tehran, or Beijing. Given the state of its finances, you’d have to have a vivid imagination to describe American government bonds as ‘safe’ or ‘risk free.’

The dollar/bond crisis in DC will cause capital flow to other alternative and ‘hard’ assets. Does that include value stocks or ‘deep value’ equities? Maybe…

The Least Efficient Market

There’s a new paper I’ll read next week before I meet with Bill and Tom in Dublin. Remember, we have a two-part strategy to the big political and geopolitical issues I’ve raised this week. First, preserve your purchasing power and your capital by staying in Maximum Safety Mode. Second, be prepared to deploy that capital in great businesses that compound returns over time…when you can buy them at the right price.

Into to mix is a new paper from Clifford Asness at AQR Capital Management. It’s called The Least Efficient Market Hypothesis. The title of the paper references one of the mainstays of mainstream financial thought, the Efficient Market Hypothesis (EMH). EMH holds that the stock market constantly and accurately incorporates all relevant known information and that stocks, as a result, are always perfectly priced.

Of course information changes all the time (although not all of those changes are meaningful nor relevant to the price of stocks). But the implication of EMH is that it's hard, if not impossible, for an individual stock picker to beat the market (or an index fund). The market is just too efficient, according to the theory.

Asness disagrees!

I’ll read the paper in full this weekend. But the crux of his argument is that technology has accelerated the distribution of bad information while also increasing (through commission free online trading) the amount of irrational trading.

The markets are neither rational nor efficient! And social media technology is a force multiplier for stupidity, amplifying the ideas of the dumbest and the loudest.

If he’s right, the upside is that the less efficient markets are at pricing great businesses, the greater advantage YOU have in buying those businesses at an attractive valuation. Stock pickers should be able to pick apart an inefficient market. In theory.

The downside is volatility. In less efficient markets, especially where holding periods for positions are shorter than ever, and technology increases emotional decision making, the day-to-day price action in a security may become completely uncoupled with its value (present OR future).

You might be right about the business, but stupid investors and stupid index funds will prevent you from being vindicated through a higher share price. The market can remain moronic longer than you can afford to stay in Maximum Safety Mode.

Like I said, I haven’t read all of the paper yet. It could be the sort of ‘sour grapes’ argument that blames index investments for the poor returns of stock picking value investors over the last twenty years. In the last two decades, liquidity is a quantity that has little respect for quality, preferring growth at any price.

Or, it could, when combined with the report on long-term returns in stocks I mentioned last week (Money Talks), be a strong argument that the other side of this debt crisis will be the single best opportunity for investors and stock pickers of your lifetime. For example, lower oil prices and higher gold prices ought to be an earnings sweet spot for well run mining companies. Stay tuned for more!

Until next week,

Dan

PS

PS The Latin inscription at the top of the Sobieski painting is ‘Non nobis Domine, non nobis, sed nomini tuo da gloriam.’ It’s from Psalm 115:1, ‘Not to us, Lord, not to us, but to your name give the glory.’ This was later adopted as the motto of the Knights Templar.

PPS If you like maps (because they can give you a different perspective on things) check out https://brilliantmaps.com. I found one this week that gave me a good laugh. And after reading this week’s research note, you may need a laugh. This is not an electoral map. It’s legal to do a particular thing in the blue states while in the red states, it’s not legal to do that particular thing. What is that particular thing? Owning a tank? Distilling your own moonshine? Marrying your cousin? The answer below…

(Legal status of raccoon ownership is in blue…by my math…there are 18 States where raccoon ownership is legal. Those 18 States have 206 total votes in the Electoral College. If California and Washington State were to legalize raccoon ownership…a coalition of 22 states with 272 electoral votes could win the Presidency under a legal raccoon ownership, single-issue platform)

Yeah, Doug Casey is One of Us. Like Bill Bonner too.

We can appreciate their success, sacrifices, time, and effort that Doug has made because the time is short as we all will eventually age - off into the sunsets.

It's gonna be a fun and interesting chat...

Love the Red/Blue map! You missed an 'l' in the link address...should be

https://brilliantmaps.com for more fun maps!