Risk on a Knife Edge

Plus the road to CBDCs, unsustainable debt, the great "Chinese Capitalism" misnomer and plenty more...

Bonner Private Research

Wednesday, November 30, 2022

Laramie, Wyoming

By Dan Denning

Greetings again from Laramie, where the Union Pacific southbound rumbles south just a few blocks away (for now, there is no rail strike and further supply chain disruption before Christmas.) We woke up to the news that former Chinese leader Jiang Zemin died overnight. Hmm.

Jiang oversaw the handover of Hong Kong to the communists in 1997. He also steered China into the World Trade Organization in 2001. This was an important date in American economic history. Along with the North American Free Trade agreement in 1995, it accelerated the destruction of the American Middle Class through a strong dollar, record trade deficits, and the decimation of American manufacturing. Jiang was 96. We’ll get back to him–and China’s history of capitalism with ‘Chinese characteristics’--in a moment.

A reminder that our founder Bill Bonner is in Baltimore. He’ll return soon. Bill’s working on a project to find out what is (and is not) working in the newsletter world. The first-ever Annual Report to the Chairman (or the Chairmen’s Letter, as we’re calling it) should be available to you (for free) in the last two weeks of December.

Philosophy, Music and Target Practice

In the meantime, all ears are on Jay Powell. It’s a demoralizing sign of the times, and of how centralized and bureaucratic the American economy has become, that we have to pay meticulous attention to the speeches, syntax, and grammar of a man who runs an unelected cartel of bankers. We could be reading Aristotle, pumping iron, learning the piano, or going to the range.

Instead, we’ll read Powell’s speech to the Brookings Institute for any sign that the Fed has softened its stance about inflation ahead of its next meeting in just a few weeks. Traders–judging by the futures market–think the Fed will raise rates to around 5% and then cut twice in 2023.

Traders are not listening to Fed officials, or at least not taking them seriously. St Louis Fed President Jim Bullard said last week that the Fed needs to raise its target rate to a range between 5% and 7% to break the back of inflation at 40-year highs. That implies that the Fed will raise rates more than expected, and then leave them there longer than expected.

Traders are big, petulant babies, though. They don’t want higher rates. Higher interest rates mean lower prices for risk assets. And that includes investment grade corporate bonds. We looked at equities and Apple yesterday. Now take a look at the chart below.

On a Knife Edge

LQD is an exchange traded fund (ETF) that tracks an index of investment grade corporate bonds. These aren’t junk bonds. They are creditworthy corporations that should, all things being equal, be able to navigate refinancing and borrowing at higher rates in 2023 and beyond. What does the chart tell you?

I’ll tell you what it tells me: that the rally in risk assets is on a knife edge. Why? A couple of things.

First, the blue line is the 100-day moving average (MA). The red line is the 200-day MA. LQD has to trade above that 100-day MA and THEN cross the 200-day MA for momentum to be bullish. Note that in July–the last massive head fake rally in risk assets–LQD did poke its head above the 100-day MA. But not for long. Lower lows were just around the corner.

Second is the Relative Strength Index (RSI), the line at the top of the chart. Any time that is near or above 70, a stock or security tends to be overbought. Any time is near or below 30, a stock tends to be oversold. LQD’s RSI was over 70 on Friday’s close.

Over $3 billion exited the $36 billion fund on Monday, according to Bloomberg. That was the biggest one-day outflow since the fund began in 2022. In a debt-deflation, liquidity seeks firmer ground, less counterparty risk, and harder assets.

A caveat: we are neither technical analysts nor chartists at Bonner Private Research. But I do use a few simple technical indicators and some basic chart analysis. Why? If the price action is different from your thesis, then either the price action is funky or your thesis is wrong. In this case, the price action confirms the thesis behind our asset allocation strategy for 2022, namely that bonds are dog excrement.

That might change in 2023. Tom Dyson (our Investment Director, for those of you new to our service) just released the November Monthly Strategy Report in the last 48 hours. We added that report recently to review, each month, our big-picture outlook on stocks, bonds, cash, gold, real estate, and crypto (all the major, and minor, asset classes).

That’s the second caveat: we are not short-term traders. We’re taking a long view of the current trades, trying to connect the dots, and coming up with a sensible and safe investment plan. Which brings me to the chart below.

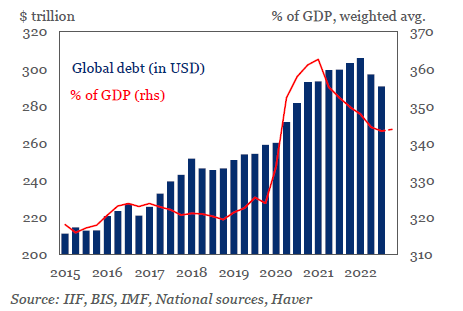

Unsustainable Debt

Total global debt has increased by $80 trillion in the last ten years, according to the Institute of International Finance. The housing bust, the Wall Street bailouts, the Covid lockdowns, every single crisis (organic or manufactured) has been met with an increase in household, corporate, and government debt. The chart above shows that debt bubble beginning to deflate.

Nominal debt peaked at $305 trillion in late 2021. As a percentage of GDP, it peaked just before that at 362%. Since then–which happened to coincide with peaking stock markets in late 2022–total debt has declined to $290 trillion. It’s now ‘just’ 343% of world GDP.

It’s always been Bill’s contention that the whole world started to go wonky when the money system changed in 1971. Everything since then has been a series of booms and busts induced by funny money. Not much–wages, the quality of information, productivity–has improved in real terms.

It’s now Tom’s contention that we’ve entered an era of ‘inflation volatility.’ That’s where central bankers try to manage the debt deflation so it doesn’t ‘break something’ in the real economy (like the housing market, for instance.) The big risk right now is that even though nominal debt levels could be declining, the interest expense on the debt outstanding is rising as interest rates rise. Pain for over-leveraged borrowers at every level.

It’s MY contention that the most over-leveraged borrower in the world is the US government. And that its interest expense is already rising rapidly. And that $1 trillion annual government debts and a $31 trillion national debt will lead to either a bond market implosion or a dollar crash. Which will then usher in a ‘new dollar’ in the form of a Central Bank Digital Currency (CBDC).

What a world of total surveillance and control of your money looks like is beyond the scope of today’s letter. Tomorrow, Bill returns with an old friend to discuss this, and other, pressing issues. And I will get to work on my Friday research note to paid subscribers about how soon a CBDC could become a reality.

Until tomorrow,

Dan

PS There is no such thing as ‘capitalism with Chinese Characteristics.’ It’s a euphemism designed to create the impression that there is a ‘third way’ between communism and capitalism and that this ‘third way’ includes long-term government planning, allocation of capital, and control of the economy. Call it socialism if you like. But it’s not a system based on sound money, private property, low taxes, and the Rule of Law.

I distinctly remember the Statists lecturing us critics of the Patriot Act that their beloved government would never abuse this additional power. The Statists claimed the critics were tin foil hat wearing conspiracy theorists. Well, we all know how that worked out. Welcome to the surveillance state :-) Now the Statists are again lecturing us critics of the CBDC claiming their beloved government would never abuse this additional power. Programmable money; what could possible go wrong :-) Your biggest enemy is not the government, its the Statists. The government needs their useful idiots and the Statists line up to fill that role. The government along with their Statist dullards are the antithesis of Liberty. Believe it or not; there's still many American's who do not enjoy bondage and chains. It really is that simple.

"the price action confirms the thesis behind our asset allocation strategy for 2022, namely that bonds are dog excrement."

Haha, right on.