Miran Contra: Is the Trump Grand Strategy Working?

It’s not that power tends to corrupt, or that absolute power corrupts absolutely (as Lord Acton famously said). It’s that power is magnetic to the corruptible.

Friday, July 17th, 2026

Laramie, Wyoming

By Dan Denning

Prediction: Now that Christopher Nolan’s cinematic version of Homer’s Odyssey is in theaters, the ‘tomato meter’ on Rotten Tomatoes will plummet–below 75% by Monday and on its way to 50% by the end of the month. All the initial ratings, which drove the score up to 98% at one point, were critics who’d seen a screening before the public. Critics are generally elitist line-toers. The Crowd will now vote. And it will be merciless.

The good news is we can now look forward to the final installment of the Dune series as re-imagined by Denis Villeneuve. Aside from some odd casting choices here and there (nothing as unabashedly ‘woke’ as the choices made by Nolan), the first two Dune movies have pretty much stuck to the book: a coming of age story in which a charismatic son avenges a murdered father and unleashes a galaxy-wide jihad on the decrepit, corrupt, and elite ruling order with an army of fanatical jihadist warriors who believe their leader fulfills a religious prophecy about the coming Paradise.

Pretty standard stuff. If you’ve read Frank Herbert’s Dune books, you’ll know that Paul Atreides isn’t the hero. He’s the villain. And even though he thinks he can find ‘a golden path’ to restore justice and peace and order in the universe, he’s wrong. History marches to its own rhythm and appoints each man his role. Paul drenches the world in blood.

The books are a warning. It’s not that power tends to corrupt, or that absolute power corrupts absolutely (as Lord Acton famously said). It’s that power is magnetic to the corruptible. Herbert wrote, ‘Power attracts pathological personalities…Such people have a tendency to become drunk on violence, a condition to which they are quickly addicted.’

We’ll see how the story ends when Dune, Part Three comes out December 18th, 2026. Until then, let us resume with our story about American power, drunk on debt. We’ll set aside liquidity and valuations this week and look at two other variables that affect our investment returns for the next ten years, policy and strategy.

To the extent that the Trump Administration has an actual strategic policy goal, we learned in 2024 that it might look like Stephen Miran’s new global currency re-set, dubbed the Mar-a-Lago Accord. The argument was simple: the use of the US dollar as a global reserve currency made it over-valued. This chronic/structural over valuation resulted in the US running large trade and government (fiscal) deficits.

From an economic point of view, the large trade deficits helped American consumers in the form of low import prices and massive choice in consumer goods, textiles, and food. But it did not benefit American manufacturing nor the inflation-adjusted hourly wages of American workers. Trump promised to get a new deal. A better one.

Miran’s paper said the US also deserved more equitable ‘burden sharing’ for the cost it has paid to protect the global order with massive military spending. American taxpayers pay for this ‘security umbrella’ (mostly by large annual deficits). It benefits Americans in the sense that the world’s goods continue to flow into the US (or did) at bargain basement prices. But Trump wanted a new deal there, too.

Miran’s solution came in three parts. First, punitive tariffs to force bi-lateral trade deals more favorable to American industry and labor. Second, make US defense and security spending conditional on better currency/trade deals. Third, impose fees on the interest payments due to foreign holders of US government debt if trade and currency deals aren’t re-arranged.

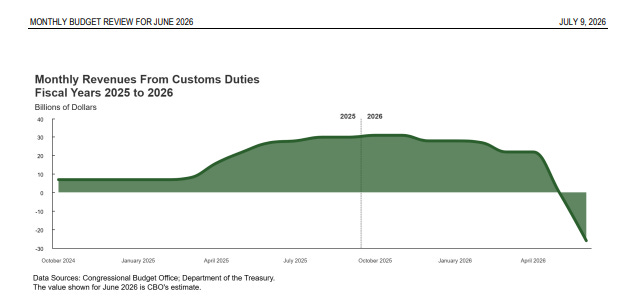

Lots of stick. A tiny bit of carrot. And to thoroughly mix the metaphor, no dice. The chart above from the Congressional Budget Office shows the US government collected $195 billion in tariff revenues in 2025. But when the Supreme Court ruled them broadly illegal earlier this year, the government began issuing rebates (it’s not clear to whom, but it’s definitely not consumers).

The Administration does have other statutory authority it can use to impose tariffs and has already done so. But the stick is limp. Tariffs are not going to generate enough revenue to eliminate the income tax (as was very briefly discussed before being discarded). Nor are they going to lead to a broad de-valuation of the dollar like the 1985 Plaza Accord devalued the Japanese yet. Speaking of the dollar.

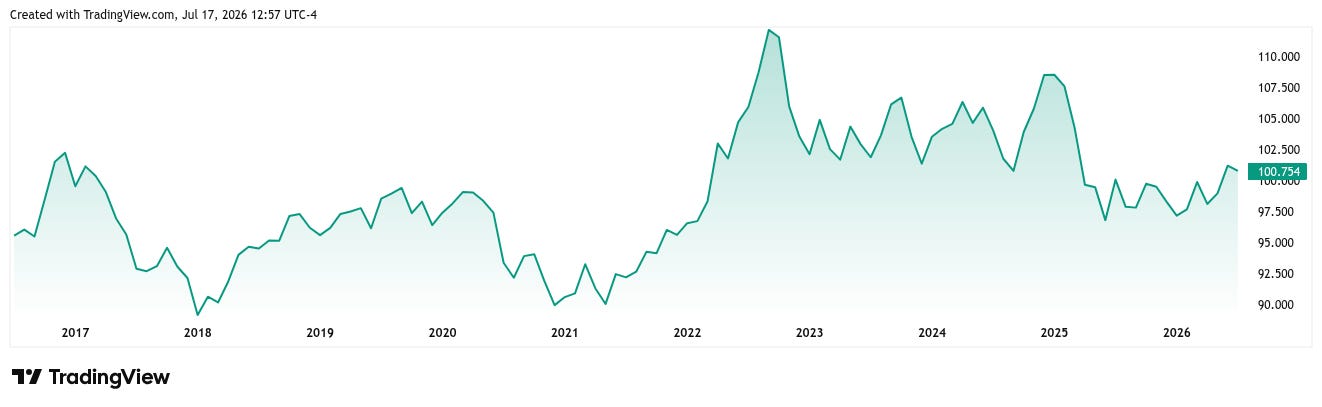

Here it is. Remember that this time last year, the US dollar was coming off its worst first-half performance in 50 years. Not since the collapse of the Bretton Woods system in 1973 had the greenback fallen by 10% in six months against its international peers.

Of course that was all part of the Miran plan. Weaken the dollar without damaging foreign demand for US government bonds. But the chart above shows that the Dollar Index [DXY] is almost exactly where it was ten years ago. Not stronger. And certainly not weak to the point where US exports would suddenly surge according to the plan.

The available evidence shows there has been no restructuring of the global trade system by fiddling with the dollar’s financial plumbing. Money moves where it wants and where it’s treated best. In the meantime, DOGE didn’t cut $2 trillion in wasteful spending (although it probably found at least that much…and Congress didn’t seem to cut any of the waste DOGE DID find). And with the war in Iran (which Congress has still not declared) military spending will go up 44% to $1.5 trillion if the President has his way.

This is the New Boss behaving a lot like the Old Bosses. No new deal for American workers. No New Dollar. No year in the sun for Main Street. Just more debt for future Americans to pay off and higher financial asset prices for Wall Street now.

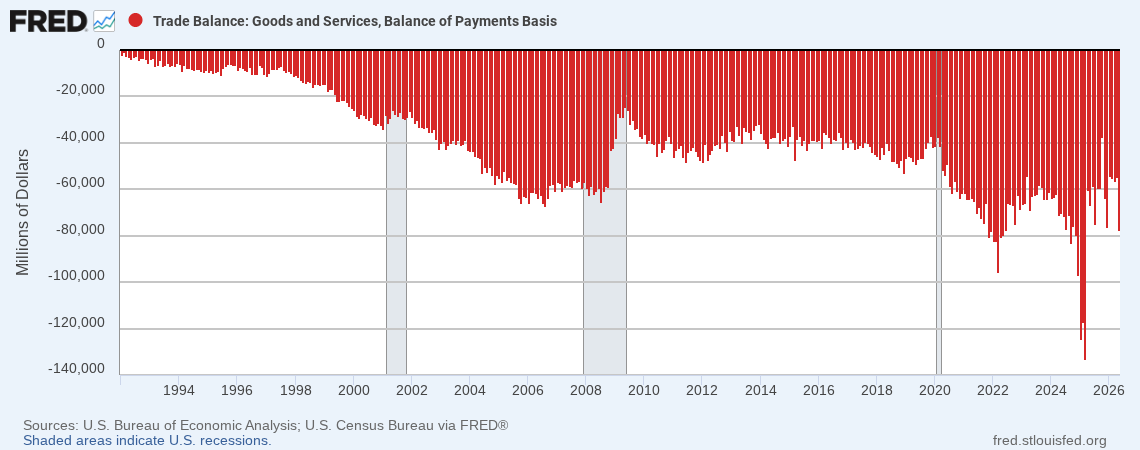

The trade deficit has not gotten smaller either. You can see it absolutely blew out in early 2025 with importers trying to front-run the tariffs and build up inventories. Since then it’s been more of the same. Month after month, America importing more than it exports.

It’s been that way for a long time. But the real decline began with Bill Clinton and a Republican Congress passing the North American Free Trade Act (NAFTA) in 1995. US political leaders from both parties made a conscious decision to favor Wall Street and the dollar (the capital account) over Main Street, manufacturing, and trade (the current account).

Deep in the details, the result is creation of one of the largest debtor nations the world has ever seen. The Net International Investment Position (NIIP) of a country tells you whether it’s a creditor or a debtor. It’s the difference between what we own versus what we owe. We owe.

The most recent numbers show the NIIP at a negative $21.2 trillion (assets of $66.64 trillion versus liabilities of $43.37 trillion). And if you can believe it, that was a $600 billion improvement over the net debtor position at the end of 2025. But that improvement came entirely from the increase in the value of foreign assets owned by Americans and not a smaller trade deficit.

A net creditor (like Japan) can afford to run a debt-to-GDP ratio over 200%. It can finance its deficits out of available domestic savings (it saves). The ONLY way a net debtor like the United States can afford to do the same—without seeing a huge spike in interest/rates and borrowing costs–is if investors see the global system as safe, basically fair, and stable.

Yet the whole intellectual basis of the Trump Trade Stategy was to make that order LESS stable….It’s a bold strategy, Cotton. Let’s see if it pays off for them.

So far, it hasn’t. And you could argue that it is un-like Trump to have a complex mechanical plan for restructuring the entire global trading system. He’s a self-styled deal-maker. And he probably thought he could get a better deal using the usual tactics he’s employed over the years—move fast, be chaotic, set unrealistic expecatations, make bombastic announcements, settle for something. Rinse. Wash. Repeat.

Only it hasn’t worked. And that begs the question, IS there a strategy?

Well on that question, the answer is probably ‘yes.’ The idea that tariffs and manufacturing are the source of a nation’s wealth, strength, and security go back all the way to Alexander Hamilton. Writing soon after the Revolution, Hamilton was worried that a nation of farmers and commodity exporters would not be able to stand up to Great European Powers for long. In his report ‘On the Subject of Manufactures,’ published in 1791, he wrote:

Not only the wealth; but the independence and security of a Country, appear to be materially connected with the prosperity of manufactures. Every nation, with a view to those great objects, ought to endeavour to possess within itself all the essentials of national supply. These comprise the means of Subsistence habitation clothing and defence.

The Trump Administration, through the investment programs at the Departments of Energy, War, Commerce, and Interior, has made a conscious effort to re-shore manufacturing in the nuclear supply chain (mining, processing and refining, next gen reactors), rare earths, and critical minerals. We’ve covered some of those stories in these pages.

Whether it results in self-sufficiency and resiliency in industries deemed critical to national security, only time will tell. The soonest any of the investments might bear fruit, according to my research, is 2028. A lot can happen in the interim.

In the meantime, it’s clear that some people in the US government (and in the industries most likely to benefit from government investment) believe the country ought to have an industrial policy. That industrial policy ought to be linked to various trading strategies. And that done correctly, all that should result in more security, a better and more self-sufficient industrial base, and higher wages for the American worker.

Maybe. It’s an idea. And this is a departure from throwing hundreds of billions of dollars toward renewable energy and hoping for a mythical ‘Energy Transition.’ That resulted in wasted money and wasted time, or at the very least, the lining of a lot of pockets from those closest to the money in Washington.

It’s certainly not the free market as we know it, though, is it? The more important question is will investors and BPR readers benefit from the Trump national industrial strategy, such as it is, and for however long it lasts?

Energy Fuels Inc. [UUUU] is a company we wrote about in May of 2024 (Nero Would Weep). Its White Mesa Mill in Utah is/was the only operating uranium mill in the country. It has a licensed capacity of eight million pounds of uranium per year. It’s the leading US producer of U308, the concentrate you need to make fuel for nuclear power plants.

It is/was a uranium play. But it’s also a rare earth play. Processing uranium is toxic partly because the ore is radioactive. You have to make all sorts of provisions for the dust generated. And you have to be in a jurisdiction/geography friendly to such endeavors. Utah is such a place.

Last month, the Department of War signed a $720 condition loan with UUUU to process monzanite ore at the White Mesa Mill. This might make it (might) a successful domestic producer of rare earth elements. That would fit nicely with the ‘Mine-to-Magnet’ strategy the Administration is pursuing. We’ll see.

The stock chart shows the thrills and perils of piggy-backing on US industrial policy. Without a 50% trailing stop, you would have been knocked out of the position twice since May of 2024 before being in the money. Then you MIGHT have tripled your money. Or suffered some massive drawdowns. It would involve a lot of tactical trading, which is not our bag.

It’s all very exciting. But it’s also well beyond our Maximum Safety mandate. Tempting with play money. And worthy of continued study. But nothing to bet the farm (or the factory) on. Especially at these prices/valuations.

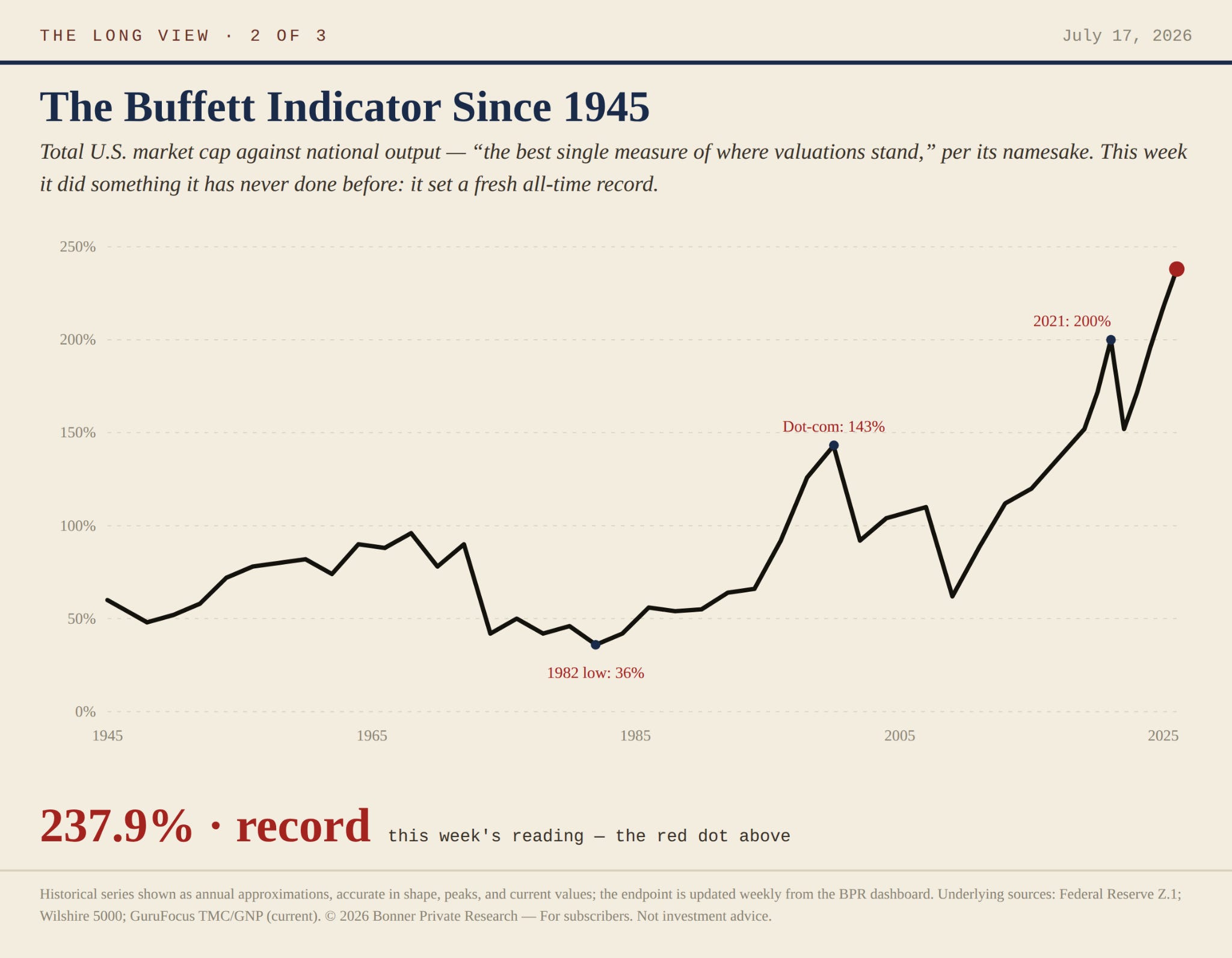

We’re making a few revisions to our dashboards to make them more visually appealing. Here’s an example above. It’s ‘the long view’ of the Buffett Indicator. Record times. Record risk. We’ll stay off stocks on the golden path for now.

Until next week,

Dan

PS We’re also looking at updating the look of the Official List. What do you think? These two images are based on Wednesday’s data (not updated for today’s close). Leave a comment below. We’ll publish the full dashboard, the BPR Reckoning Index, and the Doom Index in the upcoming August Monthly Strategy Report.