Friday, April 10th, 2026

Laramie, Wyoming

By Dan Denning

The tankers are coming! The tankers are coming!

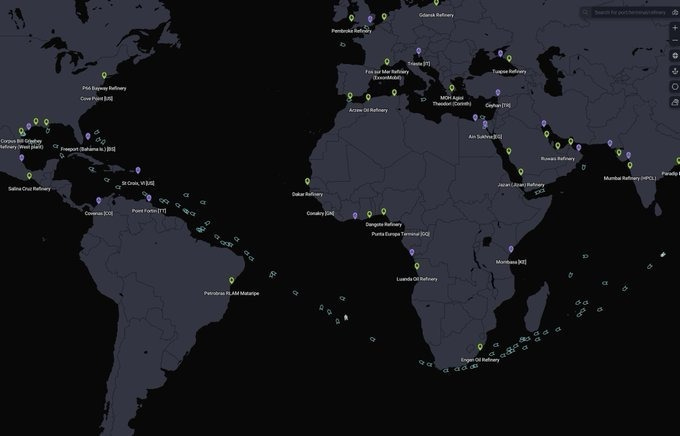

A ‘wave’ of Very Large Crude Carriers (VLCCS) are headed around the Cape of Good Hope in Africa for the Gulf Coast in America. As Tom has pointed out for a few years now, the VLCCs carry between 1.9 and 2.1 million barrels of crude oil. Please see Tom’s note from Wednesday on how to manage strength in our tanker stocks.

Normally, 80% of the oil passing through the Strait of Hormuz would be headed to Asia. The times, they ain’t a normal. Industry publications show that 40 VLCC ‘liftings’ are booked in American ports for April. The average is 27. It’s not an oil armada yet. But it does set up an interesting tension.

US exports of crude oil could be set to boom. It’s a bit of a paradox. This week’s CPI and core personal consumption expenditure data show that rising energy prices are already driving up inflation in the US. The CPI data is from March and the PCE data was from February. It’s likely to get worse (higher energy prices) before it gets better.

Yet the US is on pace to export over five million barrels of oil a day to markets that can’t get it easily from anywhere else. What are we to make of this? Is it politically tenable to endure higher energy prices in the US while exports hit new highs?

Jeff Currie from Carlyle thinks we have an emerging conflict between the ‘electrostate’ and the ‘petrostate’. Up in the air is the 50-year global bargain where the US provided a blanket of security through trillions in military spending in exchange for ‘dollar dominance’ (the recycling of oil money back into US government bonds and financial assets like stocks). Without the security, the dollar’s dominance can’t last. The bargain is ended.

You’ll recognize Currie’s name if you were around for the last commodity supercycle in the first decade of the 21st century. He ran the commodities desk at Goldman Sachs and was one of the top analysts for how the price hike, investment boom, and production boom would play out for investors (most of this was driven by huge levels of fixed asset investment in China in things like bridges, railroads, housing and airpots…while the US was bleeding trillions of dollars in the deserts of Iraq).

What he’s suggesting now is that the Strait of Hormuz is effectively closed to anyone Iran and China want to exclude. This gives China, in Currie’s analysis, global control over critical minerals, rare earths, microchips, and ‘oil access’ for countries that are not energy self-sufficient. In this environment, he forecasts a huge rotation back into heavy industry and energy. Asset heavy over capital light, if you want to put it in balance sheet terms.

Whatever you think about the thesis, it sure doesn’t look like the Strait of Hormuz is open. Or that there’s a ceasefire in hostilities. Or that there’s anything in the world that can prevent coming fuel and food shortages, driven by the disruption to global energy transportation. Some people have already felt the pain. Others will soon enough. And investors?