Jamaican Exception

Economic crises often become political crises, too. If you are lucky, people lose money... they lose their jobs... businesses and investors go broke... and that’s the end of it.

Wednesday, April 17th, 2024

Bill Bonner, reckoning today from Dublin, Ireland

Gloomy. Defeatist. So negative... even our computer got depressed and stopped working.

Over the past week or so, we’ve seen...

... that the main two things that bring down a great nation are war and debt

... that the US is not backing away from either of them

... that US debt is approaching the Doomsday Trigger of 130% of GDP

... that we all use the same credit card for public expenses... and kick the debt can down the road to someone else, some other time, to be paid off somehow

... and that in a modern democracy, the decider compete for power and money; none has an incentive to stop kicking.

Primary Trend Reversed

Let’s put these insights in context. The bond market topped out (with record low yields) in July 2020. The stock market topped out at the end of 2021. These looked to us like reversals in the Primary Trend; nothing has happened since to suggest otherwise. Most likely, we’ll see generally lower real stock and bond prices (with higher interest rates) for many years to come.

We’ve seen the Tops. Now, we await the Bottoms. As Tom points out, we’re in ‘Maximum Safety Mode.’ We’ll move back into ‘growth mode’ and sell gold when stock prices go down so low that you can buy the entire thity Dow stocks for five one-ounce gold coins.

Most likely, the US government will have to hit some kind of bottom too. It will have to get into the middle of a genuine debt crisis, before it can come out on the other side. Then, it can return to sustainable financial policies. Alas, that turnaround is nowhere in sight.

But wait. There’s always more to the story. Isn’t Javier Milei turning Argentina around? Isn’t RFK, Jr. suggesting that he will do likewise in the USA? Didn’t Jamaica successfully pull out of a debt crisis... and Greece too?

Yes, yes, yes, and maybe.

Full Sh*thole

Only a few years ago, Jamaica was on the edge of a financial breakdown. It had spent too much and borrowed too much. Lenders refused to provide more credit. Inflation was running riot. The currency was losing value.

But rather than go Full Sh*thole, Jamaica pulled up its socks and got to work. A couple of academic studies, reported in the Financial Times, tell us what happened:

Jamaica halved its government debt-to-GDP ratio from 144% between 2012 and 2023…[It] did it through sustained primary surpluses (excess of revenues over spending, excluding interest payments) exceeding seven per cent of GDP for seven straight years.

For reference, the US is currently operating with a budget deficit of about six per cent of GDP.

The authors of the academic work, professors from Stanford and Berkeley along with Serkan Arslanalp of the IMF, concluded that it was a “hard-won tradition of consensus building” that did the job for Jamaica. Somehow, the government was able to get nearly everyone to go along as it cinched the budget belt tighter and tighter.

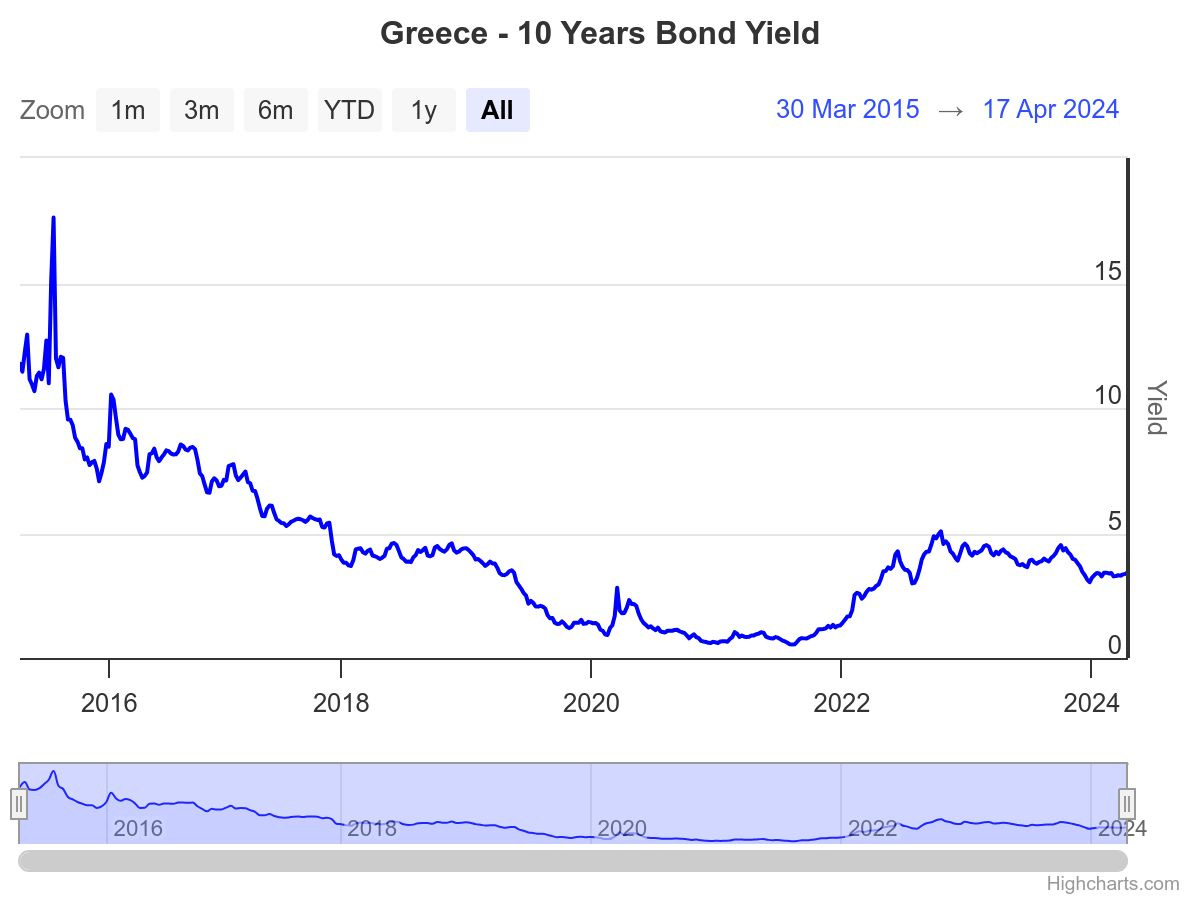

Greece is another case. We took a trip to Athens in 2015 just to see it; we wanted to see a financial collapse up close.

Greece’s public finances were absurdly mismanaged and notoriously corrupt. The government had been in “almost continual default” for the entire 19th century and much of the 20th century. It spent money it didn’t have... and then lied about its numbers so you couldn’t tell what was actually going on. In 2008, for example, its military spending was twice the EU average.

Germans vs. Greeks

But in 2009, it hit the Doomsday Trigger — with debt greater than 130% of GDP. Under normal circumstances, people might not have extended it so much credit. But Goldman Sachs had helped it disguise its real financial situation so as to gain membership in the European Union. As a member of the EU, it was able to borrow in a stable currency — the euro — and appeared to have the backing of Germany and France.

Then, when the trouble began, the Germans protested: they didn’t want to bail out the lazy, profligate Greeks. So, the Greeks did what they always did: they became the first developed nation to ever default on an IMF loan. There were riots... bank closures... chaos and turmoil.

Outlays were cut. Bailouts were negotiated. More crises. More negotiations. At one point in 2012, a 20-year Greek bond was almost worthless, with a yield spiking to nearly 140%.

Greece was a ‘basket case.’ But life went on. The ATMs didn’t work. But restaurants were open. Tourists had disappeared... so there was no trouble getting a table. Unemployment increased, but many Greeks were used to not working anyway.

In 2011, Greece was in a depression, with GDP declining at a 7% rate. More than 100,000 companies went broke and the unemployment rate hit 23%. The debt-to-GDP ratio hit 177% in 2014. And by 2016, Greece seemed to be hitting bottom, with one out of three Greeks said to live in poverty.

Tanks in the Streets

But it can get worse. Economic crises often become political crises, too. If you are lucky, people lose money... they lose their jobs... businesses and investors go broke... and that’s the end of it. If you’re unlucky, you hear the sounds of gunfire and see tanks in the streets,

So far, Greece has been lucky. It could have bolted from Europe and told the ‘Troika’ — the IMF, the World Bank, and the EU — to get lost. It could have gone back to its own currency, the drachma, as Paul Krugman advised, and gone on a bacchanalia of money-printing and hyperinflation. Instead, it buckled down... cut spending, raised taxes, fired deadbeat ‘public servants’ and actually managed a budget surplus of about four per cent of GDP.

Its debt-to-GDP ratio has come down from as much as 180% to 160%. But with the help of the Troika, it seems to be holding things together as it reduces its debt.

What can we learn from these examples? Probably not very much. They are small countries, where democracy seems to work better. And, unlike the US, they were never able to borrow large amounts in a currency whose value they controlled. So, they couldn’t “inflate away” their debts.

More to come...

Regards,

Bill Bonner

Market Note, by Dan Denning

Did you know that Greek 10-year bond yields, at 3.44%, are actually BELOW the US 10-year bond yield of 4.61%? That’s despite Greece still having a debt-to-GDP ratio of 160%. Greece doesn’t have its own printing press. But it does have the European Central Bank (ECB) to buy its bonds AND the perception that Germany won’t allow any one country to torpedo the Euro currency (we’re looking at you Italy, with a debt-to-GDP ratio of 143%).