Do the Opposite

Below you’ll find an essay published last week by our colleague Edward Bonner at Sprott Money. Please enjoy.

May 27th, 2026

Dear Reader,

It has been 82 days since the war began. In my last letter, I urged caution—favoring quality equities, cash, and oil. In the weeks that followed, markets did the opposite: the S&P 500 made new all-time highs, throwing caution to the wind.

Now, reality appears to be catching up.

We expect choppier waters heading into the seasonally weak summer months as investors adjust to higher bond yields and the possibility of renewed rate HIKES. Ultimately, however, we believe central banks will have little choice but to ease in order to support growing deficits and rising debt burdens. When that pivot comes, it should serve as the catalyst for hard assets—particularly against a backdrop of worsening structural scarcity.

In this letter, we’ll walk through the current macro environment and examine some of the most compelling opportunities today. But first, a quick note: I’ll be attending the Rule Symposium in Boca again this year. This one looks to be gearing up to be the best one yet. If you’ll be there, please shoot me a line so we can connect and share ideas.

Do The Opposite

Markets continue to behave as though geopolitical risks are contained and monetary policy will soon ease. Positioning today feels less like a debate and more like a consensus: inflation fades, rates fall, geopolitics normalize. Nice and tidy.

May’s Bank of America Fund Manager Survey reflects exactly that. Positioning is now the most bullish since January 2022. Semiconductors remain the most crowded trade (73% of respondents), and expectations for double-digit earnings growth have surged. Meanwhile, just 16% of investors foresee rate hikes in 2026, and 66% expect the Strait of Hormuz disruption to resolve within months. Only 4% of respondents expect a hard landing as cash balances have fallen sharply, from 4.3% to 3.9% - the largest monthly decline since Feb-24.

Despite one of the largest supply disruptions in modern history, equity allocations have risen at a record pace. Because why stop a good party?

The issue in crowded markets isn’t that fundamentals suddenly collapse—it’s that liquidity becomes one-sided when the narrative shifts. When flows reverse, they tend to do so quickly.

This risk is amplified by extreme concentration. Today’s index performance is increasingly driven by a narrow group of mega-cap stocks. Since the March 30th lows, roughly 70% of the S&P 500’s gains have come from just ten names. At times, the majority of stocks have moved in the opposite direction entirely.

Narrow leadership masks deteriorating breadth—and when positioning unwinds, it increases the likelihood of sharp, air-pocket declines.

Priced for Perfection

This narrow market also reflects a bifurcated economy—the so-called “K-shaped” economy. All’s well for those at the top, while those at the bottom are struggling to make ends meet. In fact, a recent survey form Goldman Sachs estimated that 41% of American households earning between $300K-$500K are living paycheck to paycheck. Hardly a sign of a healthy economy.

There is effectively no margin for error. Many segments of the market—particularly technology—are priced for perfection. Ironically, when positioning already assumes good news, even positive developments can be met with indifference… or selling.

The Shiller CAPE ratio is not a timing tool, but it is a powerful framework for setting expectations: when starting valuations are extreme, forward 15-year returns tend to be almost nil.

Ratio: Current Market Valuations - Lyn Alden")

Valuations are so out of whack, Berkshire Hathaway now holds roughly 32% of its assets in cash, representing about 5% of the entire U.S. Treasury bill market. Here’s Buffett speaking at the annual shareholder meeting in Omaha: “It isn’t our ideal surrounding area or environment... in terms of deploying cash for Berkshire.” Adding: “The most likely time to buy things is when nobody else will answer their phones.”

So for now, we wait. Eventually, something’s gotta give.

Under Pressure

Recent inflation data suggests that pressure is building again. Both CPI and PPI surprised to the upside, reinforcing the “sticky inflation” narrative. Energy alone accounted for roughly 40% of the CPI surprise, while PPI strength points to continued pipeline pressures—particularly within services. And you can be sure these will eventually be flowing to the end consumer.

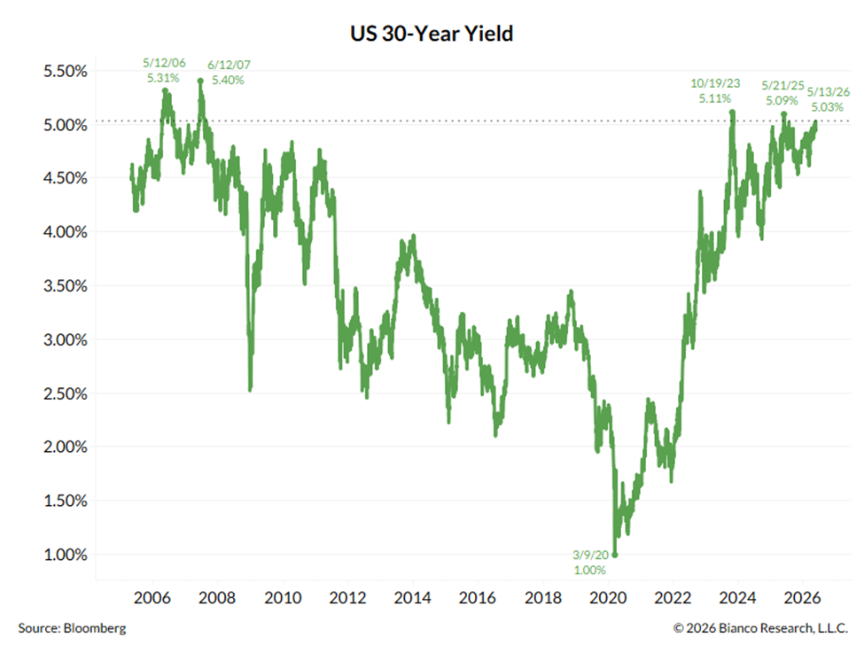

As a result, long-end yields are once again testing critical levels. The U.S. 30-year yield recently touched 5.19%—its highest level since 2007. Japan’s 30Y yield hit an all-time high of 4.17% and across the G7, long-term yields are spiking, with the 10Y surpassing the 2008 Financial Crisis peak.

Technically, the long end of the curve is pressing against resistance. Repeated tests of this ~5% level raise the probability of a breakout—particularly if inflation remains persistent or if investors demand higher term premia to finance growing deficits.

A sustained move higher in long-end yields would tighten financial conditions, compress valuation multiples, and increase the risk of a rapid, flow-driven de-risking event. In short, it would reintroduce friction into a market that has grown accustomed to operating without it.

Running on Oil

Energy remains the key swing factor—both for inflation and rates.

And there is little relief in sight.

With the Strait largely closed, roughly 20% of global oil supply has been disrupted. For context, the 1973 oil embargo removed approximately 4.5 million barrels per day from the market. Today’s disruption is closer to 20 million barrels per day—three to four times larger in volume terms.

Despite a more resilient modern market structure, the current level of optimism appears misplaced.

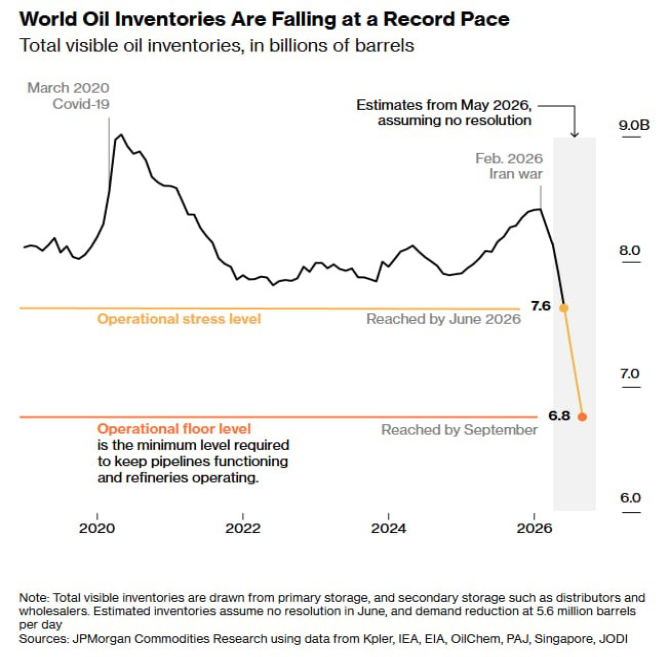

Oil markets have begun pricing deficits—but not yet outright shortages. As seasonal demand increases, that distinction may become critical. Already, major producers, such as Qatar Energy, Kuwait Petroleum Corp, and Bahrain’s Bapco Energy, have declared force majeure, and global inventories are drawing down at a record pace.

Strategic reserves offer limited relief. After accounting for recent exchange agreements with major oil producers, by August U.S. SPR levels could be at their lowest level since the early 1980s (roughly around 280Mbbls). And replenishment isn’t likely until winter—assuming no further disruptions.

The situation is dire. And the pinch is being felt all over the world. Global oil inventories are depleting at record pace. Our market strategist writes: “Sometime in early June operational stress will be very evident.” Heaven forbid this lasts until September…

Even in a best-case scenario where the Strait reopens, normalization will take time. Infrastructure damage, delayed shipments, labor constraints, and elevated insurance costs all point to a prolonged recovery. As Saudi Aramco’s CEO recently noted, a full return to pre-conflict supply levels may not occur until well into 2027.

Getting Scarce

It’s a challenging backdrop—but not without opportunity.

If broad equity indices offer limited upside from current levels, where should investors look?

We continue to favor commodities and real assets, where the risk-reward asymmetry remains compelling. The setup is defined by tightening supply, rising demand, and increasing strategic competition for resources.

The energy transition is accelerating, driving sustained demand for copper, nickel, silver, uranium, tungsten, rare earths, and other critical materials you’ve probably never heard of. At the same time, supply remains constrained by years of underinvestment, permitting challenges, and geopolitical complexity.

Scarcity is no longer a theory—it is becoming embedded in the system.

Demand is being reinforced on multiple fronts:

Structurally, through electrification and renewable buildout

Politically, through supply chain security and strategic stockpiling

Monetarily, through rising debt burdens and the long-term risk of currency debasement

Together, these forces create a durable tailwind for real assets. Some more than others.

Go Gold

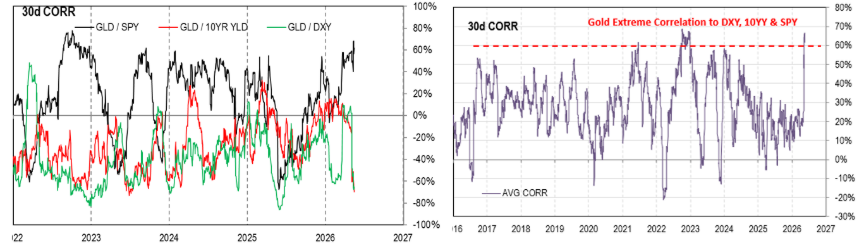

In the near term, gold may face some pressure.

Macro correlations between gold, equities, yields, and the U.S. dollar are near extreme levels—suggesting positioning is heavily dominated by systematic flows. If yields and the dollar move higher, gold could see a short-term pullback as algorithms de-risk.

However, this dynamic is unlikely to persist. When central banks eventually pivot to stabilize bond markets, gold should respond accordingly—much as it did following similar conditions in 2022.

In other words, any weakness should be viewed as an opportunity within a broader structural bull market.

The Opportunity

We remain cautious on broad equity markets given extreme concentration, crowded positioning, and a rates backdrop that may prove less forgiving than the consensus expects.

At the same time, we see a compelling opportunity set in scarcity-driven assets and commodity-linked equities, where fundamentals are supported by multi-year supply deficits and durable demand growth.

One area where we’ve been actively leaning into this theme is our private placement fund. Over the past several months, we’ve participated in more than a dozen financings—often in companies that are difficult to access through traditional public markets and remain underfollowed.

Performance since inception has been strong, and we would be happy to share further details upon request. We invite you to reach out for a discussion about suitability and how this exposure may complement a broader natural resource allocation.

As always, I am available for a call if you have questions about your portfolio.

Best regards,

Edward

Edward Bonner

Investment Advisor, Geologist

Direct: +1 760 444-5262

ebonner@sprottglobal.com

Important Disclosure

Relative to other sectors, precious metals and natural resources investments have higher headline risk and are more sensitive to changes in economic data, political or regulatory events, and underlying commodity price fluctuations. Risks related to extraction, storage and liquidity should also be considered.

Gold is referred to with terms of art like store of value, safe haven and safe asset. These terms should not be construed to guarantee any form of investment safety. While “safe” assets like precious metals, Treasuries, money market funds and cash generally do not carry a high risk of loss relative to other asset classes, any asset may lose value, which may involve the complete loss of invested principal.

Past performance is no guarantee of future results. You cannot invest directly in an index. Investments, commentary, and opinions are unique and may not be reflective of any other Sprott entity or affiliate. Forward-looking language should not be construed as predictive. While third-party sources are believed to be reliable, Sprott makes no guarantee as to their accuracy or timeliness. This information does not constitute an offer or solicitation and may not be relied upon or considered to be the rendering of tax, legal, accounting or professional advice.

Thanks so much for sharing Edward!

Talking your book