Joel Bowman, checking in today from Buenos Aires, Argentina...

“Trust your own eyes. Not the damned lies.”

So warned Bonner Private Research’s Dan Denning to members earlier this week.

Dan was referring to the fed’s fiddling with the inflation figures... as is their wont. (Yes, yes, gentle reader... you are positively shocked to discover public officials up to no good, we know.) Here’s Dan, with the skinny...

The benign consumer price inflation (CPI) figures from November and December were bogus. Okay. Maybe ‘bogus’ is unfair. But bear with me.

CPI numbers for both months were revised higher this week by the Bureau of Labor Statistics. In November of last year, CPI increased 0.2% instead of the previously reported 0.1%. And in December, CPI increased by 0.1% rather than the previously reported decline of 0.1%. Does it really matter?

It depends on if you took the numbers seriously in the first place. A small difference here and there can be an honest statistical revision by a diligent bureaucrat buried somewhere in the bowels of a Washington office building. Or, it could be deliberate misinformation to manage stock market expectations...

Real World Prices

We tracked a few items in yesterday’s missive (under Bill’s hilarious “Burning Crow” story). Measured against real money – gold – the greenback lost 0.4% of its purchasing power in 2022… and this despite one of the most aggressive rate hike campaigns in recent history. It’s lost another 2% so far in 2023, even as Mr. Powell’s Fed remains committed to fighting the very inflation they didn’t see coming and then largely ignored when it inevitably arrived.

After a raging start to 2022, the dollar index (DXY) has been in steady decline from its high of 114 in October last year. It closed yesterday’s session at 103 and change...a 9.6% fall from its fall peak.

Of course, gold is but one tape against which to measure the dollar’s terminal atrophy. Stack your USDs up against airfares… or a dozen eggs… or school lunches… and see how far they stretch (or don’t).

The aforementioned items were up 28.5%… 59.9%… and (incredibly enough) 305% in dollar terms during 2022, a year that saw inflation rip to a four decade high.

The dollar simpered against other real world items last year, too. Flour was 23.4% more expensive in dollar terms… lettuce was up 24.9%… butter by 31.4%… and margarine by 43.8%. Overall, the cost of eating at home rose 11.8%. As for dining out, many working Americans – squeezed by rising costs on the one hand… and falling real wages on the other – simply can’t afford the luxury. (Though we doubt Mr. Powell or Ms. Yellen will be missing a lobster lunch anytime soon…)

Dan has more on the inflation story below... including the “sticky” kind... as in, “non-transitory.” But first, let’s take a quick peek at the past week in the markets, shall we?

Major indexes finished mixed on Friday, with the Dow Jones Industrial Average up half a percent, the S&P 500 higher by 0.2% and the Nasdaq lower by 0.6%. The latter was not helped by ride-sharing company, Lyft, which reported weak earnings Friday and subsequently tumbled more than 36% for the session.

Over the week, all three major indices finished lower, the first time that’s happened since December. The Dow dipped 0.17%, while The S&P 500 fell 1.11% and the Nasdaq Composite lost 2.41%. Year to date, all three are squarely in positive territory, up 2.2%, 6.9% and 12.8%, respectively.

Gold ended the week more or less where it began, at around $1,865/oz. One factor keeping a floor under the price, at least according to Rupert Rowling, market analyst at Kinesis Money, is central bank buying.

“One factor that could well be keeping the gold price so supported,” said Rowling in an interview, “is the strength of buying from central banks, including those in China, India and Turkey. As these fast-growing economies look to diversify away from the hegemony of the US dollar, these banks have bought considerable volume last year with that trend expected to continue into this year.”

Central banks to citizens of the world: CBDCs for thee... gold for me!

Over in the energy markets, oil seems to be holding steady around $80/barrel (WTI).

And in the crypto world, leader of the pack, Bitcoin, dropped almost 5% on the week. It was last seen hovering around $21,700. Even so, it’s up over 30% year to date. By the time you read these words... it could be anywhere.

But let’s get back to the real world prices most people pay most days of the week. Dan, again…

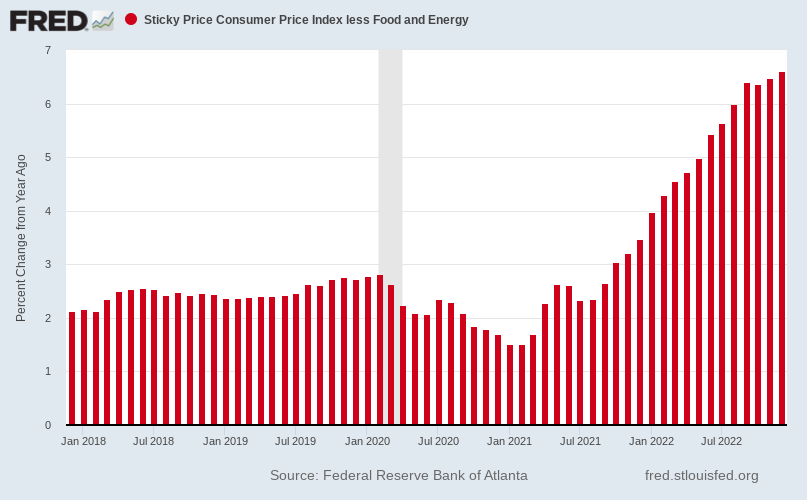

Below is a five-year chart of ‘sticky’ consumer price inflation I wrote about last month (members can view the original research here: The Velocity of Desperation). Sticky prices don’t change as much, which means they aren’t as volatile (and less likely to be statistically excluded from the monthly calculation). And because they change less frequently, they also have a bigger influence (according to the Fed’s own researchers) on consumer inflation expectations.

(Source: US Federal Reserve)

The ‘sticky’ number is not moderating. It is not showing ‘disinflationary tendencies.’ It’s proving stubborn. It’s proving that the government can change how it measures inflation. But that doesn’t reduce actual inflation, or change the public perception that prices are rising. Changing how you measure prices doesn’t make food or energy cheaper either.

The point of sound money–keeping the purchasing power of the dollar stable–is that you don’t have to believe in prices, or attribute their rise to anchovies, China, or Putin. Sond money produces prices that don’t require belief. They only require voluntary consent, between a buyer and a seller, content in the knowledge that the medium of exchange isn’t going to rob one or the other of their labor, money, or time.

That’s probably a quaint notion in these days of distortion. But keep it in mind next week when the CPI numbers come out. Trust your own eyes. Not the damned lies.

For those following along at home, the CPI print is due out Tuesday. No doubt Dan and Tom will be on the case with their analysis of the situation as it evolves/devolves.

Speaking of which, Tom sent his regular update to members on Wednesday. Included was this snippet...

The federal government has been running large deficits for most of the last 50 years. But then central banks created a world where cash had no yield… and in some cases it had a negative yield. It was toxic… like trash. You were punished for holding it. And so everyone fought to get rid of their cash. They bought whatever they could with it… anything with a yield.

It’s all a big experiment. Proponents said it would lead to a strong economy and plenty of jobs. But I think it just temporarily stimulated consumption and speculation and the mirage of wealth.

Because of its size and duration, I think it’s fair to call this experiment the greatest financial experiment in all human history.

And now, interest rates are suddenly nearing 5%. It’s been the fastest, most aggressive rate hiking campaign in 40 years. And it may still have further to run. I wonder, what idiotic speculations did people make when rates were at zero percent and they were fighting to get rid of their cash? And when will those trades be unwound?

Maybe it’ll all turn out fine. Maybe it will end in a spectacular collapse and liquidation… a financial conflagration...

With all the weight of economic history behind us, the smart investment move here is to let this bear market run its course. These big trends always take much longer than you expect to get started. But when they move, they move quickly.

Slowly at first. Then all at once.

“Our strategy for 2023 is simple,” concluded Tom. “We don’t have a clear view of how things will play out this year. So we simply stand aside, on the sidelines, and watch the spectacle from a safe distance. Then we try to earn some safe income.”

As of Wednesday’s update, there were eight (8) open positions in the Bonner Private Research Official Stock Watchlist, with an average return of 24.6%. If you’d like to follow along with Tom and Dan’s strategy, standing clear of the growling bear while trying to earn a little income along the way, you can do so by finding a membership program that works for you, right here...

One has to ask oneself, why are all central banks stocking up on gold like China and Russia have been doing for many past years? Could it be the World Bank wants to base our future world CBDC on the gold standard? Just maybe raising the price to well over $20,000 an ounce to pay off the old debt? Hey, you never know, and still a great time to buy the pretty yellow metal 😊

One has to ask oneself, why are all central banks stocking up on gold like China and Russia have been doing for many past years? Could it be the World Bank wants to base our future world CBDC on the gold standard? Just maybe raising the price to well over $20,000 an ounce to pay off the old debt? Hey, you never know, and still a great time to buy the pretty yellow metal 😊