Breaking Math

Speculators buy into bubbles, not investors. In the bubble psychology, speculators believe that they can buy high...and sell even higher.

Tuesday, April 28th, 2026

Bill Bonner, from Baltimore, Maryland

The South China Morning Post reports:

Will China’s mathematicians join a global effort to boycott the United States?

America’s tech prowess — AI included — is built on a foundation of numbers.

So, the International Congress of Mathematicians is a big deal. It’s scheduled to meet in Philadelphia in July. But America’s tough visa rules and its war on Iran have inspired more than 2,300 mathematicians to sign a petition to “move the 2026 ICM out of the US.”

Does it matter? We don’t know. But it is just one of many signs that the world is moving away from us. And here’s more, The Conversation:

‘China’s rapid rise in science has hit a milestone. The country’s investment in research and development has reached parity with — and by purchasing power measures has surpassed — that of the United States, according to a March 2026 report from the Organisation for Economic Co-operation and Development. Both nations have crossed the US$1 trillion threshold on research spending.’

But so far, investors worldwide have not turned their backs on US equities...even though those stocks are at the top of bubble territory...and even though no bubble has ever failed to pop.

The question we left you with yesterday was: how come the bubble hasn’t popped? Is this something new, an eternal bubble? A smile that never turns to a frown? It seems unnatural...like mac without the cheese...a bender without a hangover...the Resurrection without the Crucifixion.

The eternal bubble idea came to us just as words. But mathematicians know why it isn’t possible. Our newest and bestest friend — an unpaid researcher, Claude — told us so. Claude is, of course, an AI app, freely available on the internet. And there is almost nothing that Claude doesn’t know.

Why can’t we have a bubble without tears, we asked him. Claude:

Bubbles pop because the conditions that inflate them are self-undermining.

The same dynamics that drive prices far above any reasonable estimate of underlying value also guarantee that the rise can’t continue indefinitely.

The arithmetic eventually breaks. A bubble requires prices to keep rising fast enough to reward new buyers. But sustaining, say, 30% annual gains compounds into absurdity within a decade — the asset would consume the entire economy. At some point the implied future earnings, rents, or cash flows become mathematically impossible, and even committed believers run out of ways to justify the next leg up.

In other words, what makes a bubble a bubble is that it is unusual. The things in it go up at an extraordinary pace. But as Claude points out, it is mathematically impossible for that to continue for very long. Nothing can grow at an extraordinary rate forever. Because it would soon fill the universe. There would be no room for anything but the extraordinary thing, which would make it very ordinary.

But why couldn’t the bubble just remain as it is? Claude might be worn out from his mental exertion already, so we’ll answer the question ourselves.

Investors don’t buy into a bubble, looking forward to the dividend checks. As they say on Wall Street, “you make your money when you buy.” And buying high means that the anticipated earnings per share will be relatively low.

Speculators buy into bubbles, not investors. In the bubble psychology, speculators believe that they can buy high...and sell even higher. They believe, often correctly, that when others see how well they are doing, they will want to join the party too.

But eventually the math doesn’t work. The bar closes and they turn off the music. Then, the speculators, who might have borrowed money to bet on the bubble, will be disappointed....and under pressure. They can ‘do the numbers’ too. If they have borrowed at 5% interest, even a 4% gain leaves them feeling blue.

Stable prices work for investors; not for speculators. When the music stops and a bubble no longer acts like a bubble, speculators go home. Not only does a stagnant bubble make them no money...it also poses substantial risk of big losses.

Speculators, after all, are betting on capital gains, not earnings. So, they are very alert to capital losses, too. And when a bubble seems to level off, they know what is likely to happen next.

First, the mathematicians edge for the exits. And then they all skedaddle.

Regards,

Bill Bonner

Research Note, by Dan Denning

Reinvested dividends accounted for more than 50% of the total return in US stocks in the 20th century. That data and analysis comes from a book called Triumph of the Optimists, published in 2002. It’s based on annual data from the Credit Suisse/UBS Annual Global Investment returns yearbook.

The 50% figure comes from the combination of several things. First, time is on your side when it comes to compounding. The longer you do it, the more you make. Reinvested dividends grow the total return faster than capital gains alone (higher prices). But that’s not all.

US companies paid dividends as a reward to investors willing to take the risk of owning stocks ‘for the long run.’ It was compensation in the form of cash returned to shareholders as income, and taxed at a favorable (lower) rate than capital gains. It’s important to note the 50% figure from the Triumph dataset is both cumulative (not annualized) and inflation adjusted (a real return, not a nominal return).

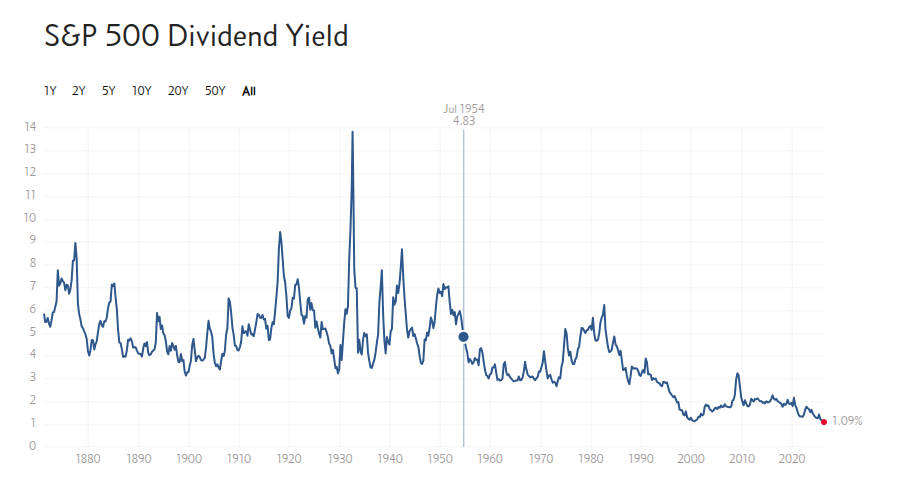

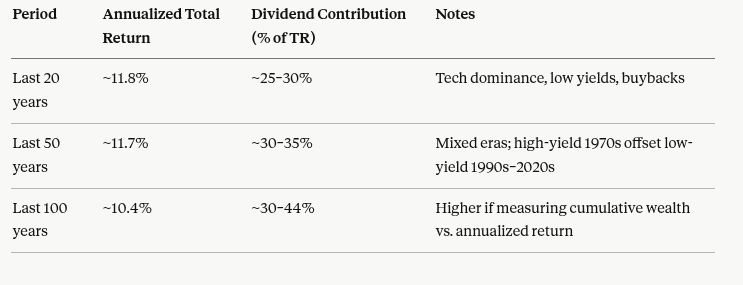

The S&P’s own figure for the total return of the index in the last 80 years is around 44% (not adjusted for inflation). But broken down into 20, 50, and 100 year increments, the data show that dividends contribute less to the total return on the index than they used to. In the last 20 years, reinvested dividends only account for about 25% of the total return. In the last 50 years, 35%, and the last 100 years, around 44%, according to S&P. Why does this matter for investors right now?

A low dividend yield is a valuation metric. It tells you to expect below average inflation adjusted returns for the next five to ten years. When investors have become accustomed to expecting big annual price gains in stocks, they stop looking for income. Historically, that happens near the end of a bubble.

The term ‘shareholder yield’ has replaced ‘dividend yield’ with some value investors. Shareholder yield counts dividends paid to investors. But it includes stock buy-backs as well. The idea is that it’s the broadest measure of cash that is returned to owners (in one way or another).

As you might guess, the ‘shareholder yield’ is higher than the old ‘dividend yield’ on the S&P 500. But even the shareholder yield is historically low, around 3-4%, well below its historical average (it’s harder to crunch buy-back data over time). Not even aggressive corporate stock buybacks have been enough to push it higher.

In the May Monthly Strategy Report out tomorrow, Investment Director Tom Dyson will update paid subscribers on the income stocks on the BPR Official List. Tom dropped a note late last night about one of his recent oil and gas picks getting a buyout offer in the last 24 hours. Stay tuned for news and further recommendations tomorrow.

Foreign enrollment in the various tech departments at Purdue University is at an all-time high. I guess these people are getting visas and matriculating (and paying list-price tuition in the process) so they can abandon the USA later. Our problem is not that international mathematicians are shunning America; our problem is that half of the domestic electorate is determined to kill what's left of her. Best always. PM

I think today's note is supportive of staying with metals and energy and selling off any stocks we have that have made us money. Metals will always have value and "black gold" will drive the world for at least 50 more years and probably longer. As I've read many times (and lost $ because of it) , I've lost money by falling in love with what I thought was a good long term stock. Bad decision!

Jim Marshall