A Huge Mistake

Saving is suspect. Scrooge saved his money. Jesus tells of a master, who berated his servant, for saving his money rather than investing it. And King Midas, turning everything into gold, starved.

Friday, January 16th, 2026

Bill Bonner, from Baltimore, Maryland

Having despaired at trying to figure out what Mr. Trump is...we look at what he is not in order to see what is not coming. We’ve tried several labels for Donald Trump. The only one that seemed to stick was ‘capitalist,’ but of an antique variety...relatively rare in today’s world.

A real, modern capitalist uses savings to provide a product or a service that is worth more than the labor and materials (the capital) that went into it. Thus, he ends up with more capital...and the world is a richer place. Win…win.

This is the process that Adam Smith described in the Wealth of Nations. The capitalist seeks to make money for himself, but he does so by making things better for others. This is also at the heart of modern — New Testament era — morality in which we are taught to ‘do unto others as we would have them do unto us.’ We want others to give us soup and shelter; we need to figure out what we can give in exchange. That is the only ‘equality’ that societies can actually provide — an equal and smiling respect for the ‘golden rule’ that benefits everyone.

Industrial economies, beginning in the 19th century, made these free exchanges possible on a vast scale. And in the rough and tumble of turn-of-the-century (1900) industry...people, in the aggregate, prospered. The Titans of industry, however, became fabulously wealthy. Those titans — Ford, Rockefeller, Vanderbilt, et al — got rich by providing lots of autos, fuel, transportation and so forth.

Then, along came John Maynard Keynes. In his Treatise on Money 1930, he made the startling claim that money was not an innocent bystander. Eerily prescient, but staggeringly off base, he claimed that rich people preferred to hoard their wealth in the financial economy, rather than spend it or invest it in the industrial economy, leading to depression and unemployment.

Saving has always been suspect. Scrooge saved his money. Jesus tells of a master, who berated his servant, for saving his money rather than investing it. And King Midas, turning everything into gold, starved to death.

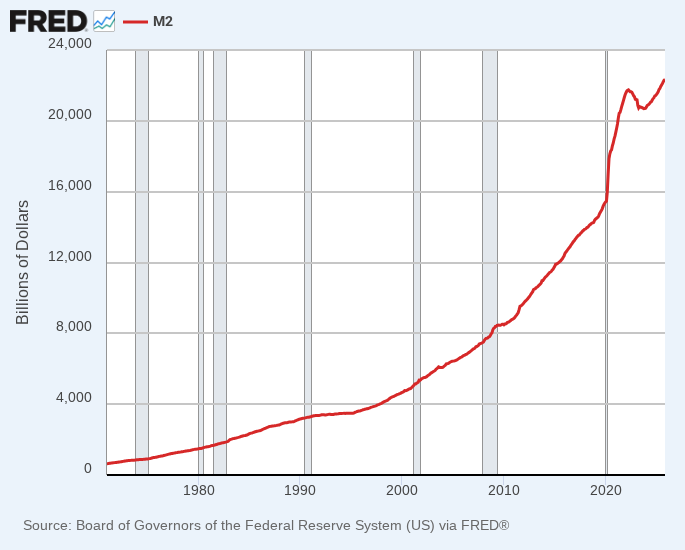

This ancient prejudice helped to justify the 1971 sleight of hand that switched real money with ‘paper’ money. The post-1971 dollar solves Keynes’ problem. There is no ‘liquidity preference’ for this new money. Just the opposite. There’s an illiquidity preference, a desire to get rid of it before it loses value.

The old money was ‘slow’ money. It took time to earn it...forbearance to save it...care and study to invest it...and often decades for it to pay off. But this new money was ‘fast’ money. It could be created in seconds...and then used in a speculation that might pay off in hours...days...or weeks. Its titans were from Wall Street, not Detroit or Gary, Indiana. They did not necessarily add to the world’s wealth. Part of the ‘bubble economy,’ not the industrial economy, they were money manipulators...leveraged speculators…and the Donald J. Trumps. Even Warren Buffett, who invests in the ‘industrial’ economy, owes much of his fortune to the bubble money that drove up prices for the last 43 years.

The available money supply is a combination of the quantity of it, along with the speed by which it changes hands. That was Keynes’s complaint against gold; people tended to hold it too long, he said. Not so this new money. The faster it changes hands, the faster each unit goes down in value.

Up until now, the ‘debasement’ of the dollar — the loss of value caused by increases in the available money supply — has been shared with much of the world. Other countries use the dollar as a reserve currency, saving it (and thus off-setting the worst effects of over-supply.)

As Putin observes, the ‘huge mistake’ of Team Trump was to upset this happy hustle by using the paper dollar, not only to cover its excess spending, but also to force other nations to do its bidding.

The US must now enforce its ‘exorbitant privilege’ — the ability to ‘print’ money and export the inevitable inflation – with kidnappings, murder and war.

Have you connected the dots, dear reader?

Not many leaders would have made the ‘huge mistake.’ Even fewer would be willing to go to war to try to head off its consequences.

But Donald Trump is a creature of this new post-1971 dollar system. And now he is its number one protector.

So, what is it that he absolutely, positively cannot do?

Stay tuned.

Regards,

Bill Bonner

Another "unprecdented Trump innovation" that turns out to have many precedents. A summary for the ahistorical:

The United States began to “weaponize” the financial payments system in a recognizable modern sense during the Second World War and early Cold War, then transformed it into a central instrument of power with post‑1970s sanctions law and, after 9/11, with dollar‑ and SWIFT‑centric financial controls that now reach the entire global banking network. What began as wartime asset freezes and trade embargoes has evolved into a dense, permanent machinery of primary and secondary sanctions that can cut states, firms, and individuals off from the dollar and from cross‑border payments altogether.

Early foundations (1917–1950s)

In 1917 Congress passed the Trading with the Enemy Act (TWEA), giving the president power to regulate or prohibit financial transactions with foreign enemies in wartime, laying the core legal basis for asset freezes and payment controls.

During the Great Depression and World War II, Franklin Roosevelt used TWEA’s section 5(b) to shut banks in 1933 and then to freeze European assets, creating a precedent for peacetime and pre‑war financial blocking as a tool of foreign policy.

Institutionalization of sanctions (Cold War era)

After 1945, the United States created specialized bureaucratic machinery, culminating in the Treasury Department’s Office of Foreign Assets Control (OFAC), to administer trade and financial sanctions as routine policy instruments rather than ad hoc wartime measures.

The Cold War saw long‑running sanctions regimes against countries like Cuba and Vietnam that combined trade restrictions with broad blocking of financial transactions and dollar payments, foreshadowing later, more targeted financial warfare.

From trade embargoes to financial leverage (1970s–1990s)

In the 1970s and 1980s, Congress embedded automatic sanctions triggers into laws such as amendments to the Foreign Assistance Act and Trade Act, mandating economic and financial penalties for human‑rights abuses, terrorism, and narcotics, thereby expanding the situations in which financial tools had to be used.

The Reagan administration’s attempts to apply “secondary sanctions” extraterritorially—such as restricting re‑exports of U.S. technology to the Soviet Union and pressuring European firms over the Soviet gas pipeline—marked an early effort to extend control beyond U.S. territory into allied financial and commercial decisions.

Post‑9/11 financial weaponization

After the attacks of 11 September 2001, the U.S. built a new model of financial warfare: instead of only blocking specific accounts or trade, it designated individuals, banks, and entities on Specially Designated Nationals (SDN) lists and threatened any bank that dealt with them, effectively turning the global banking system into an enforcement arm.

Because most global trade and finance is invoiced or cleared in dollars through U.S.‑linked banks, these measures allow Washington to make foreign banks and firms choose between access to the U.S. financial system and dealings with sanctioned parties, giving sanctions the character of a precision coercive tool with global reach.

SWIFT, secondary sanctions, and today’s system

The United States has leveraged both dollar clearing and the SWIFT messaging network—whose infrastructure and data flows are partially exposed to U.S. legal and regulatory authority—to amplify its ability to monitor and interrupt cross‑border payments, even when no U.S. party is directly involved.

Since at least the 2010s, Washington has repeatedly threatened or used sanctions that target foreign banks and infrastructures (e.g., over Iranian banking and later Russian banks), making access to the dollar payments system and SWIFT contingent on alignment with U.S. geopolitical aims and prompting widespread discussion of “weaponization of the dollar.”

Bill, enjoyed your cogent comments today. The printing of dollars kicks the can farther down the road and makes us all poorer in the long run, as well polluting other industrialized economies given the hegemony of the dollar. The result of this less than perseient behavior has been the rise of BRICS and the Chinese Belt and Road initiative. The Great Reset is in motion and it will not be good for Americans.